- Deadline arrives for Canada’s agreement to NAFTA

- Next round of US/Chinese tariffs and new threats could come late next week

- U.S. consumer sentiment expected to be revised slightly higher

- Chicago PMI expected to fall back from very strong levels

Deadline arrives for Canada’s agreement to NAFTA — The markets are waiting to see if Canada agrees to a new NAFTA agreement by today’s U.S.-imposed deadline. Both sides seem to want a deal and are delivering some compromises.

Only an agreement in principle by Friday is necessary to satisfy the notification requirements of Congress. The details of the agreement do not need to be delivered to Congress for 30 days, which means there is room to declare a victory on an agreement today while dealing with some details later.

If Canada does not join the agreement by today, then the Trump administration has said that it will give notice to Congress of a new US/Mexican trade agreement. It remains unclear whether Congress would approve a new bilateral US/Mexican trade agreement versus a revised NAFTA agreement.

If Canada does not join the revised US/Mexico NAFTA agreement by today, then President Trump has threatened to slap a 25% tariff on Canadian autos. That would cause a significant hit to Canada’s economy and Prime Minister Trudeau would likely retaliate with tariffs on U.S. products. The markets would obviously react badly if Canada crashes out of NAFTA and the U.S. and Canada then get into a bruising trade war. On the other hand, if the U.S., Mexico, and Canada can all agree on a new NAFTA treaty, the markets will be very pleased to have a major source of uncertainty lifted.

Next round of US/Chinese tariffs and new threats could come late next week — The markets are facing the possibility of a major escalation of the US/China trade war as soon as late next week. The Trump administration late next week could announce 10-25% tariffs on another $200 billion of Chinese products once the public comment period is over next Thursday (Sep 6).

If the U.S. proceeds with that tariff, then China has already said that it will levy tariffs on another $60 billion of U.S. goods. China’s proposed retaliation on another $60 billion of U.S. products would mean that China would have penalty tariffs on nearly all U.S. exports to China (including LNG) except for crude oil and large aircraft.

The mid-level US/Chinese trade talks last week ended without any progress. There are no reports of any US/Chinese trade talks to try to avert the next round of tariffs. President Trump earlier this week said that China wants to talk about trade but that now is not the right time. The Trump administration seems to want China to incur more pain before resuming negotiations.

If the U.S. tariffs on another $200 billion of Chinese products do not bring China to the negotiating table with sufficient concessions, then President Trump has already indicated that he is willing to slap a tariff on the remaining $250+ billion of Chinese products imported by the U.S. That threat could also come next week.

If the September tariff round goes into effect, then the U.S. would have a penalty tariff on $250 billion worth of Chinese goods, accounting for nearly half of the $525 billion of U.S imports from China seen over the last 12 months. China would have a penalty tariff on a total of $110 billion of U.S. products, representing about 80% of the $135 billion of Chinese imports from the U.S. seen over the last 12 months.

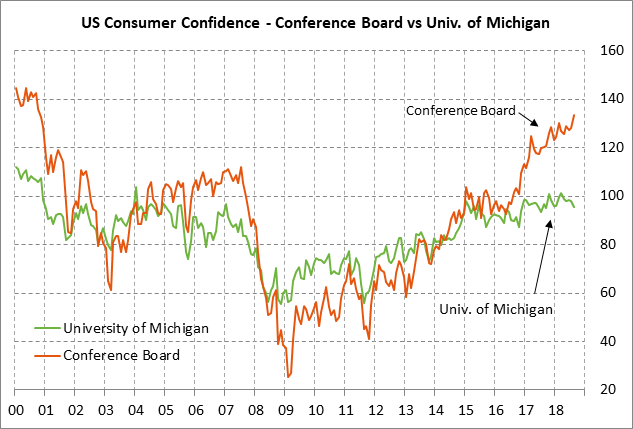

U.S. consumer sentiment expected to be revised slightly higher — The market consensus is for today’s final-Aug University of Michigan U.S. consumer sentiment index to show a small +0.2 increase to 95.5. That would leave the final-Aug index down by -2.4 points from July rather than the larger preliminary decline of -2.6 points. The index fell to an 11-month low in early August and is now down by a total of -6.1 points from March’s 14-1/2 year high of 101.4.

Concern about the weak University of Michigan U.S. consumer sentiment index, however, is counterbalanced by the fact that the Conference Board’s index is showing strength. The Conference Board’s U.S. consumer confidence index was reported earlier this week at +5.5 points to a new 18-year high of 133.4.

U.S. consumer confidence is seeing strength from (1) the strong U.S. economy and labor market, (2) rising consumer wages and income, and (3) rising household wealth due to the strength in home prices and the U.S. stock market. Negative factors for consumer confidence include (1) Washington political strife, (2) worries about tariffs and higher prices, and (3) high gasoline prices.

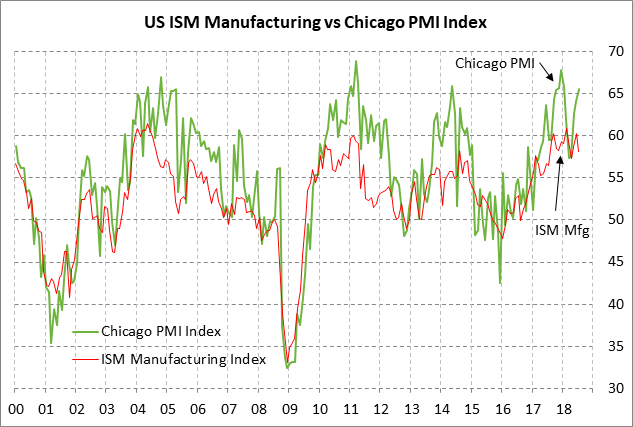

Chicago PMI expected to fall back from very strong levels — The market consensus is for today’s Aug Chicago PMI to show a -2.5 point decline to 63.0, more than reversing July’s +1.4 point increase to 65.5. The strong Chicago PMI level of 65.5 in July was only 2.3 points below December’s 7-1/4 year high of 67.8, illustrating strong optimism among manufacturing executives in the Chicago area.

On the national front, the consensus is for Tuesday’s Aug ISM manufacturing index to show a -0.7 point decline to 57.4, adding to July’s -2.1 decline to 58.1. Manufacturing confidence is taking at least a temporary hit from concerns about tariffs and the strength in the dollar. However, U.S. manufacturing confidence remains strong in general due to the very strong U.S. economy and the generally solid growth overseas. In addition, the order pipeline still looks very positive since the Aug ISM new orders sub-index was strong at 60.2 in July even after a -3.3 point decline.