- Fed’s Beige Book is expected to show a strong U.S. economy that demands more Fed rate hikes

- PPI expected to remain near recent 6-3/4 year high

- 10-year T-note yield rises to 5-week high ahead of today’s auction

- Weekly EIA report

Fed’s Beige Book is expected to show a strong U.S. economy that demands more Fed rate hikes — The Fed today will release its Beige Book survey of the U.S. regional economies. The last Beige Book released on July 18 reported that, “Economic activity continued to expand across the United States, with 10 of the 12 Federal Reserve Districts reporting moderate or modest growth…. Manufacturers in all Districts expressed concern about tariffs and in many Districts reported higher prices and supply disruptions that they attributed to the new trade policies. All Districts reported that labor markets were tight and many said that the inability to find workers constrained growth.”

The last Beige Book covered the tail end of Q2 when U.S. GDP showed very strong growth of +4.2%. That growth was the result of strength in consumer spending and business investment, which in turn was supported by improved cash flow from the Jan 1 tax cuts. Q2 GDP was also supported by a big spurt in soybean sales as Chinese buyers tried to beat China’s retaliatory tariffs.

The consensus is for U.S. GDP in the second half of 2018 to remain relatively strong at +3.0% in Q3 and +2.8% in Q4, but then to fade to +2.5% in 2019 and +1.9% in 2020 as the effects from the Jan 1 tax cuts dissipate and as the Fed’s rate hikes bite harder into the economy.

The market is discounting a 100% chance that the FOMC at its next meeting in two weeks (Sep 25-26) will raise its funds rate target by another +25 bp to 2.00%/2.25%. The market is then discounting an 84% chance that the FOMC at its last meeting of the year on Dec 18-19 will implement the fourth rate hike of the year to 2.25%/2.50%.

The market for 2019 is then discounting about 1-1/2 rate hikes (36 bp of rate hikes), which would bring the funds rate target to 2.68% by the end of 2019. That is 22 bp below the Fed’s estimate of a long-term neutral funds rate of 2.9%.

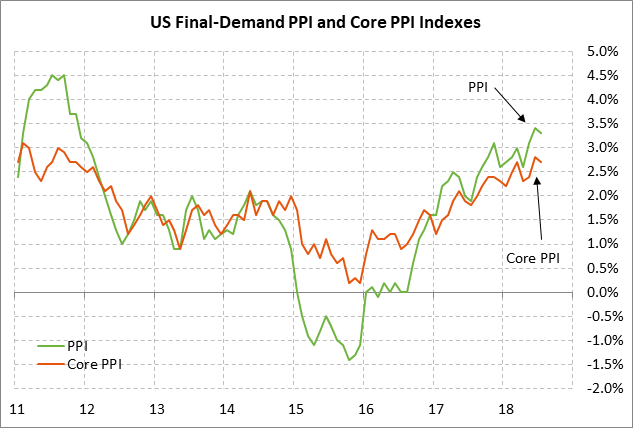

PPI expected to remain near recent 6-3/4 year high — The market is expecting today’s Aug PPI report and tomorrow’s CPI report to be little changed, which would be positive in the sense that the inflation statistics would at least not rise to new cyclical highs. The market became more worried about inflation after last Friday’s 9-year high in the Aug average hourly earnings report of +2.9% and after yesterday’s 1-month high in the 10-year breakeven inflation expectations rate of 2.12%. The good news is that the Fed’s preferred inflation measure is still near its +2.0% target with the July PCE deflator at +2.2% y/y and the core deflator at +1.9% y/y.

The market consensus is for today’s Aug final-demand PPI to ease slightly to +3.2% y/y from July’s +3.3% and for the core PPI to be unchanged from July’s +2.7%. The July PPI of +3.3% y/y was only 0.1 point below June’s 6-3/4 year high of +3.4%. The July core PPI of +2.7% y/y was only 0.1 point below June’s 6-3/4 year high of +2.8%.

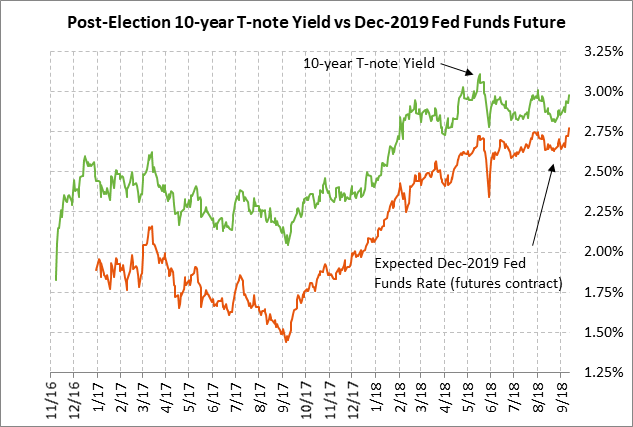

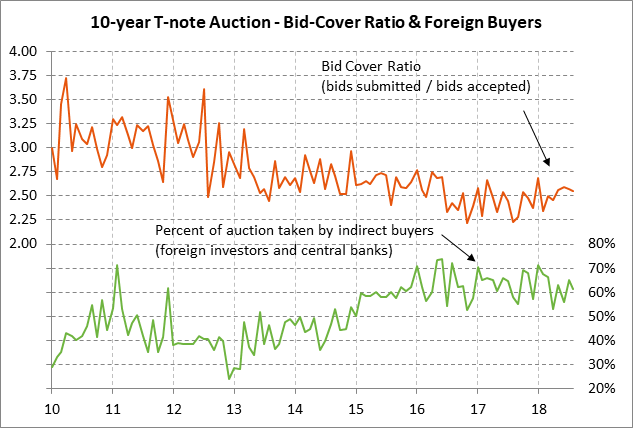

10-year T-note yield rises to 5-week high ahead of today’s auction — The Treasury today will sell $23 billion of 10-year T-notes in the first reopening of August’s 2-7/8% 10-year T-note of August 2028. The Treasury will then conclude this week’s $73 billion coupon package by selling $15 billion of reopened 30-year T-bonds on Thursday. The $23 billion size of today’s 10-year T-note is up by $1 billion from the June-July reopenings and is up by $3 billion from the $20 billion reopening size seen during most of 2016/17.

The 10-year T-note yield has risen sharply by nearly 20 bp in the past two weeks and reached a 5-week high of 2.976% on Tuesday. Factors pushing the 10-year yield higher include (1) last Tuesday’s surprisingly strong Aug ISM manufacturing index report of +3.2 points to a 14-year high of 61.3, (2) last Friday’s stronger-than-expected Aug payroll report of +201,000, and (3) last Friday’s stronger-than-expected increase in Aug average hourly earnings to a 9-year high of +2.9% y/y.

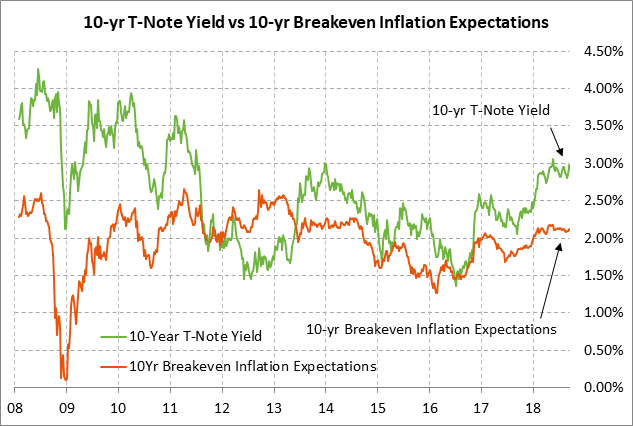

The 10-year T-note yield was also pushed higher by the +3.5 bp jump in the 10-year breakeven inflation expectations rate seen since last Friday to a new 1-month high of 2.12% on Tuesday. The breakeven rate has risen due to last Friday’s strong earnings report and Tuesday’s sharp +2.53% rally in Oct crude oil prices.

The current 10-year T-note yield level of 2.98% is only 15 bp below May’s 7-1/4 year high of 3.13%. The T-note yield fell back from that high in May, and has since consolidated below that low, mainly because of trade tensions and concerns about whether Italy will disrupt the Eurozone.

The 12-auction averages for the 10-year are as follows: 2.49 bid cover ratio, $19 million in non-competitive bids, 4.7 bp tail to the median yield, 19.1 bp tail to the low yield, and 48% taken at the high yield. The 10-year T-note is of average popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 62.8% of the last twelve 10-year T-note auctions, which exactly matches the median of 62.8% for all recent Treasury coupon auctions.

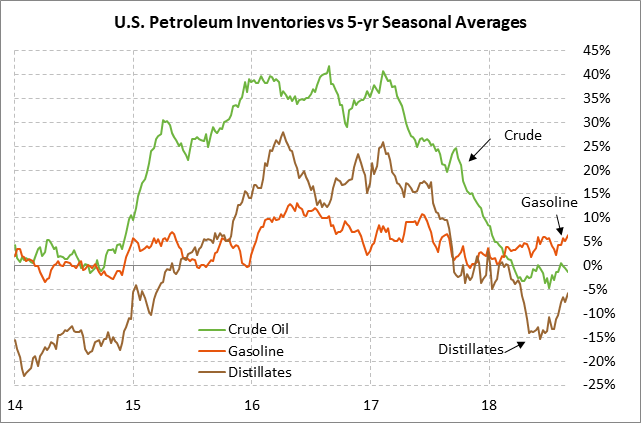

Weekly EIA report — The market consensus for today’s weekly EIA report is for a -2.2 million bbl drop in U.S. crude oil inventories, a +750,000 bbl increase in gasoline inventories, a +2.0 million bbl rise in distillate inventories, and a -0.6 point drop in the refinery utilization rate to 96.0%. U.S. crude oil inventories are currently -1.4% below the 5-year seasonal average, while gasoline inventories are +6.4% above average and distillate inventories are -5.8% below average. U.S. crude oil production in last week’s report was at a record high of 11.0 million bpd.