- FOMC unanimously expected to raise rates on Wednesday

- U.S. consumer confidence expected to remain very strong near 17-3/4 year high

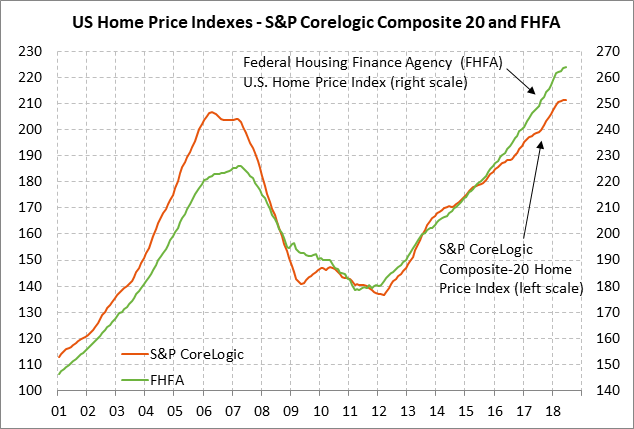

- U.S. home prices expected to continue higher

- 5-year T-note is near 9-1/4 year high ahead of today’s auction

FOMC unanimously expected to raise rates on Wednesday — The market is discounting a 100% chance that the FOMC at its 2-day meeting that begins today will raise its funds rate target by another +25 bp to 2.00%/2.25% for its third rate hike of the year. The Fed so far this year has followed a schedule of raising rates at every other FOMC meeting. The FOMC’s last rate hike was in June and the FOMC then left rates unchanged at its last meeting on July 31/Aug 1, meaning the FOMC is therefore due for its next rate hike this week based on its recent pattern. In addition, Fed Chair Powell will give a press conference after this week’s meeting, meaning he will have a chance to explain the expected rate hike.

Since a rate hike is a done deal, the main excitement about this week’s meeting comes in what the FOMC may indicate for the future in its post-meeting statement, the updated Fed dots, and the Powell press conference.

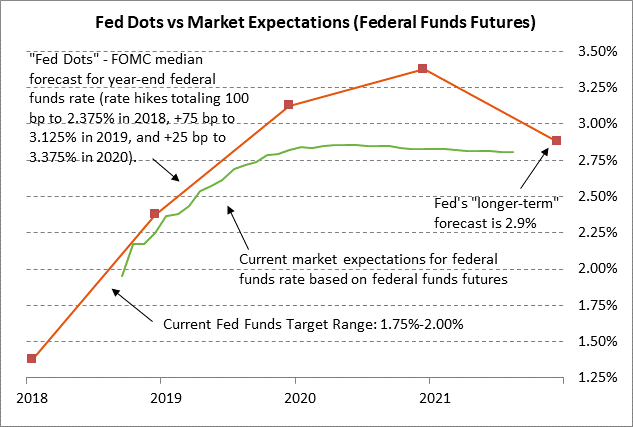

The market is discounting nearly a 100% chance that the FOMC at the meeting after next on December 18-19 will implement its fourth rate hike of the year, which would bring the funds rate to 2.25%/2.50%. The big question after that is whether the market is correct in expecting only a further 50 bp rate hike in 2019 before the Fed halts its rate-hike regime with the funds rate target near 2.82%.

The Fed, by contrast, is 50 bp more hawkish than the market, anticipating 75 bp of rate hikes in 2019 and another 25 bp rate hike in 2020, leaving the funds rate at 3.38% by the end of 2020. That is roughly 50 bp higher than the market’s terminal rate of 2.83% and the Fed’s estimate of a neutral funds rate of 2.90%.

The Fed currently believes that macroeconomic conditions are tight enough that it will have to raise the funds rate about 50 bp above the neutral funds rate to curb the economy and inflation. The market, by contrast, thinks the Fed will stop tightening with the funds near the neutral rate of 2.9%. By next year, the U.S. economy may face more challenging times as this year’s tax cut wears off and as trade tensions take a toll on the U.S. and global economies. If the market is right, the Fed will have only three more rate hikes left after this week’s hike.

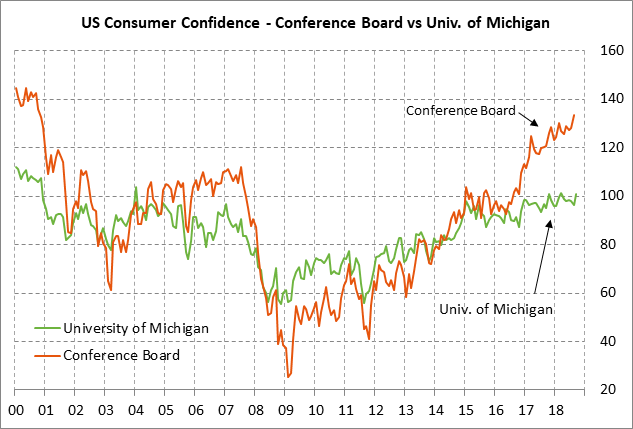

U.S. consumer confidence expected to remain very strong near 17-3/4 year high — The market consensus is for today’s Sep Conference Board U.S. consumer confidence index to show a -1.4 point decline to 132.0, reversing part of August’s +5.5 point increase to a 17-3/4 year high of 133.4. A small decline from August’s 17-3/4 year high would not be surprising and would still leave U.S. consumer confidence in very good shape.

U.S. consumer confidence is being supported by (1) the very strong U.S. economy with Q2 GDP growth of +4.2%, (2) the strong labor market with the unemployment rate near a 5-decade low, (3) strong personal income with growth of +4.7% y/y in July, and (4) rising household wealth with the record highs in the stock market and the sharp post-recession rise in home prices. Negative factors for consumer confidence include (1) the Fed’s rate-hike regime and rising mortgage rates, (2) political uncertainty in Washington, and (3) high gasoline prices.

U.S. home prices expected to continue higher — The market is expecting modest increases in home prices in today’s reports. The consensus is for today’s July FHFA U.S. house price index to show an increase of +0.3% m/m, adding to June’s +0.2% increase. Meanwhile, the July S&P CoreLogic composite-20 home price index is expected to show a smaller increase of +0.1% m/m, matching June’s increase.

Home prices have been very strong in recent months with the FHFA index in June up +6.5% y/y and up by +48% from the housing-bust trough. The S&P CoreLogic Composite 20 index, which measures home prices in the top 20 metropolitan areas, rose by +6.4% y/y in June and by +54.0% from the housing-bust trough.

However, home prices may now be due for a pause based on softer home sales and reduced demand. Homes in June were at their least affordable level in nearly ten years due to the sharp 47% rise in the FHFA’s U.S. home price index from the housing-bust trough and rising mortgage rates. The current 30-year mortgage rate of 4.65% is only 1 bp below May’s 7-1/2 year high of 4.66%.

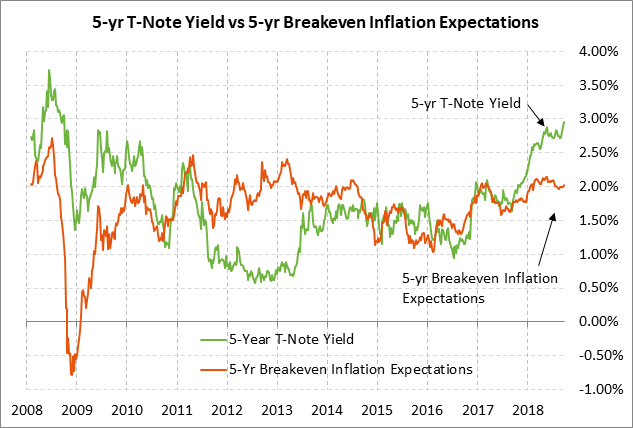

5-year T-note is near 9-1/4 year high ahead of today’s auction — The Treasury today will sell $17 billion of 2-year floating-rate notes and $38 billion of 5-year T-notes. The Treasury will then conclude this week’s $123 billion T-note package by selling $31 billion of 7-year T-notes on Thursday. The $38 billion size of today’s 5-year T-note auction is up by $1 billion from last month’s auction size and is up by $4 billion from the $34 billion size that prevailed during 2016/17.

Today’s 5-year T-note issue was trading at 2.97% in when-issued trading late yesterday afternoon, nearly matching last Thursday’s 9-1/4 year high of 2.976%. The 5-year T-note yield translates to an inflation-adjusted yield of 0.94% against the current 5-year breakeven inflation expectations rate of 2.03%.

The 12-auction averages for the 5-year are as follows: 2.49 bid cover ratio, $55 million in non-competitive bids to mostly retail investors, 4.3 bp tail to the median yield, 20.1 bp tail to the low yield, and 51% taken at the high yield. The 5-year is slightly below average in popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 62.8% of the twelve 5-year auctions, which is mildly below the median of 63.5% for all recent Treasury coupon auctions.