- Weekly U.S. market focus

- European focus remains on Brexit and Italian budget

- Asian focus remains on Chinese stocks and US/Chinese trade relations

- U.S. stocks remain on shaky ground but see support from lower interest rates

Weekly U.S. market focus — The U.S. markets during this holiday-shortened week will focus on (1) the prospects for the Trump/Xi meeting at the G-20 meeting in Argentina in just 1-1/2 weeks (Nov 30/Dec 1), (2) the prospects for the U.S. holiday shopping season as Black Friday arrives this week, (3) the heavy slate of U.S. economic data on Wednesday, (4) whether corporate bond yield spreads continue to widen on credit worries caused by the Fed’s rate-hike regime, GE’s turmoil, and the plunge in oil prices (since the oil sector accounts for a substantial weight in the U.S. high yield bond indices), (5) crude oil prices and whether OPEC+ at its meeting in 2-1/2 weeks (Dec 6) implements a sizeable production cut for 2019, and (6) whether there will be a partial U.S. government shutdown when the continuing resolution expires in 2-1/2 weeks (Dec 7).

The markets are only mildly concerned about the possibility of a partial U.S. government shutdown in 2-1/2 weeks when the continuing resolution expires on Dec 7. The shutdown would involve only a few major agencies such as the IRS, Department of Homeland Security, and the National Park service since funding has already been approved through September 2019 for most of the rest of the government.

President Trump told reporters over the weekend that, “This would be a very good time to do a shutdown.” However, Congress already plans to include some money for border security (that can be pitched as wall funding) in their current Dec 7 funding plan. In addition, Senate Majority leader McConnell said last Thursday after meeting with the President that “we’re optimistic we have a way forward” and that he doesn’t expect a government shutdown.

European focus remains on Brexit and Italian budget –The European markets this week will continue to focus mainly on Brexit and the Italian budget showdown. In addition, Friday’s Eurozone Nov flash manufacturing PMI is expected to show that manufacturing confidence stabilized in November with an unchanged PMI of 52.0 after Oct’s large -1.2 point decline.

Regarding Brexit, the markets are waiting to see if Prime Minister May’s Brexit separation agreement lasts long enough to get approved at this coming Sunday’s expected emergency EU summit. Ms. May cannot afford many more resignations from her government and several of her cabinet members are working on an alternative Brexit plan. The markets are also waiting to see whether the no-confidence movement against Ms. May’s leadership gains enough steam to get a vote in Parliament. There is a great deal of doubt at this point that Ms. May’s Brexit plan will be approved by Parliament at their expected vote in early to mid December.

Regarding Italy’s budget, the European Commission this Wednesday is due to release an assessment of EU country budgets. The Commission could bring forward an assessment of Italy’s budget from next spring that would highlight Italy’s violation of EU budget rules and kick off the disciplinary procedure that could eventually result in a fine on Italy of at least 0.2% of GDP. Meanwhile, Italy’s government is likely to move forward with getting its 2019 budget approved by the Italian legislature without any concessions to the European Commission.

Asian focus remains on Chinese stocks and US/Chinese trade relations — In Asia, the focus continues to be on Chinese stocks and the prospects for the G-20 Trump/Xi meeting. The Shanghai Composite index last Friday rallied to a 5-week high and closed the week up +3.09% on hopes for a Trump/Xi breakthrough at their G-20 meeting. Chinese stocks also received support from lower Chinese interest rates and an easier PBOC policy.

The Chinese 1-year government bond yield has now plunged by -35 bp since late October to last Friday’s 2-year low of 2.55%, which is actually 11 bp below the U.S. 12-month T-bill yield of 2.66%. Likewise, China’s 10-year government bond yield has fallen by -24 bp since late October to last Friday’s 1-1/2 year low of 3.36%, which is only 30 bp above the U.S. 10-year T-note yield of 3.06%.

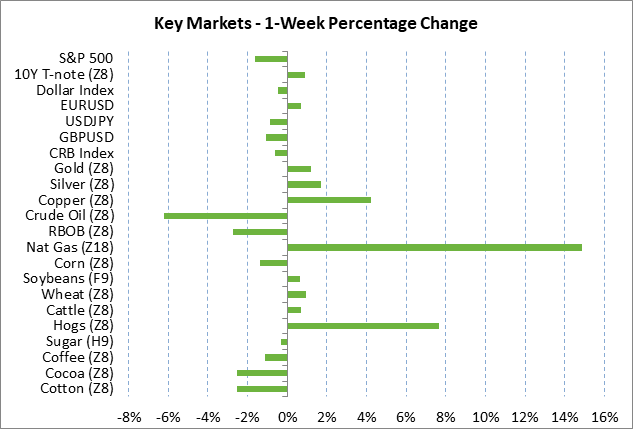

U.S. stocks remain on shaky ground but see support from lower interest rates — The S&P 500 index last Friday recovered moderately from last Thursday’s 2-1/2 week low but still closed the week down -1.61%. U.S. stocks were undercut last week by (1) the Brexit drama, (2) continued weakness in tech stocks, (3) weakness in energy stocks as Dec WTI crude oil closed the week sharply lower by -6.20%, (4) concern about the slower global economy, and (5) general trade tensions and worries about whether NAFTA 2.0 will be able to get through Congress in 2019 after a key Democratic Congressman said that he would call for renegotiation of certain provisions.

Yet U.S. stocks are seeing underlying support from (1) the more reasonable SPX forward P/E ratio of 16.7 (vs the 10-yr avg of 15.8), (2) hopes for a Trump/Xi trade ceasefire agreement at their G-20 meeting, and (3) lower U.S. interest rates and reduced expectations for Fed rate hikes in 2019.

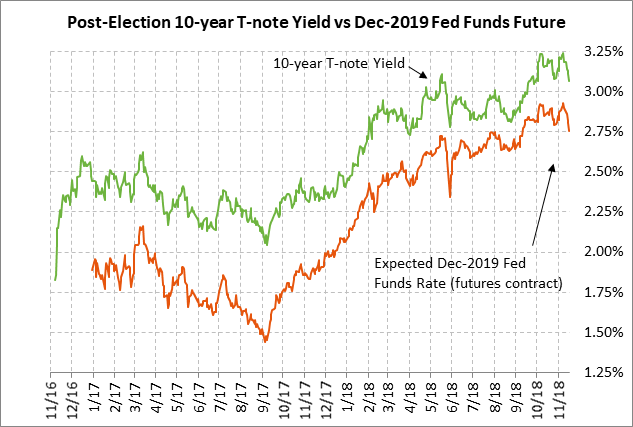

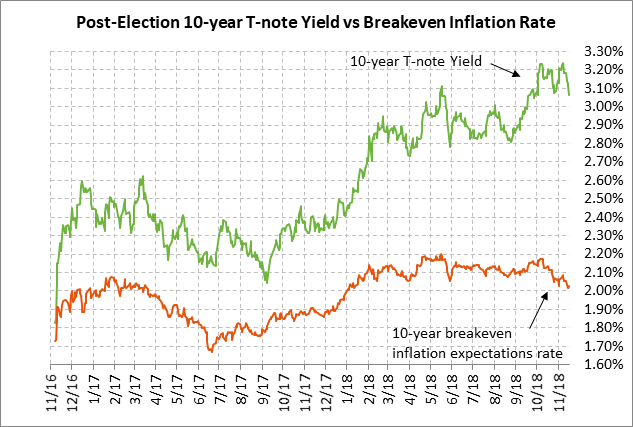

The T-note market was encouraged by Fed Chair Powell’s comments last week in which he seemed to suggest that the Fed would consider curbing its rate-hike regime in 2019 due to the slower global economy and other policy uncertainties. The federal funds futures market is now expecting only another 63 bp of Fed rate hikes through the end of 2019 (38 bp excluding this December’s expected 25 bp hike), which is down by -17 bp from the peak of 80.5 bp seen as recently as Nov 8. In addition, the 10-year breakeven inflation expectations rate has fallen sharply by -15 bp since early-Oct to 2.03%. The 10-year T-note yield has been able to drop sharply due to reduced Fed rate-hike expectations and lower inflation expectations. Specifically, the 10-year T-note yield last week fell sharply by -12 bp to 3.06%, the lowest close in 6 weeks.