- Kudlow says no recent progress on Chinese trade talks

- Report says U.S. may announce auto tariffs as soon as next week

- U.S. GDP expected to ease in coming quarters after no Q3 revision today

- U.S. new home sales expected to snap 4-month losing streak

- 7-year T-note auction yield near 2-1/4 month low

Kudlow says no recent progress on Chinese trade talks — White House economic advisor Kudlow on Tuesday said that recent talks between the U.S. and China have made no progress in the run-up to Saturday’s Trump/Xi meeting. Yet, Mr. Kudlow said that President Trump believes “there is a good possibility that we can make a deal” and he “is open to it.”

It remains unclear whether Mr. Kudlow was just trying to lower expectations for the meeting or whether the lack of any recent progress means the odds of an agreement are actually fairly low. The good news is that market expectations were low when European Commission President Juncker met with Mr. Trump back in July and yet they emerged from their meeting with a US/EU cease-fire trade agreement.

While President Trump and his advisors have talked tough about the upcoming meeting with President Xi, the fact remains that Mr. Trump needs a US/Chinese trade ceasefire if he wants to stabilize the U.S. stock market.

If Saturday’s meeting does not produce a cease-fire or framework agreement, then the U.S. stock market is likely to open sharply lower on Monday morning since the markets will expect Mr. Trump to proceed with his recent tariff threats. Mr. Trump on Monday said, “If we don’t make a deal, then I’m going to put the $267 billion additional on” at a tariff rate of either 10% or 25%. Mr. Trump also said that it was “highly unlikely” that he would agree to China’s request that he hold off on raising the tariff to 25% from 10% on Jan 1 on $200 billion of Chinese goods.

Report says U.S. may announce auto tariffs as soon as next week — European auto stocks took a hit on Tuesday after the German business magazine WirtschaftsWoche reported that European Trade Commissioner Cecilia Malmstrom would travel to Washington this week to try to head off U.S. auto tariffs, which the magazine earlier said could be imposed as early as next week after the G-20 meeting. Both the EU and U.S. Commerce Department denied the reports. The Commerce Department said it has not yet delivered its report to President Trump on whether auto tariffs are justified based on national security grounds. Nevertheless, Volkswagen and Daimler on Tuesday both fell by -2.4% and BMW fell -1.3%.

If the U.S. goes ahead with tariffs on auto imports from the EU and Japan, that would likely blow up the current ceasefire agreements that Mr. Trump has with the EU and Japan. Ms. Malmstrom recently warned that the EU is ready with retaliatory tariffs if the U.S. slaps tariffs on European autos. If Mr. Trump excludes the EU and Japan from any auto import tariffs, and also excludes Canada and Mexico (per NAFTA 2.0) and South Korea (per the US/South Korean free trade agreement), then Mr. Trump’s auto import tariffs would actually land on very few vehicles since nearly all of U.S. auto imports come from those countries.

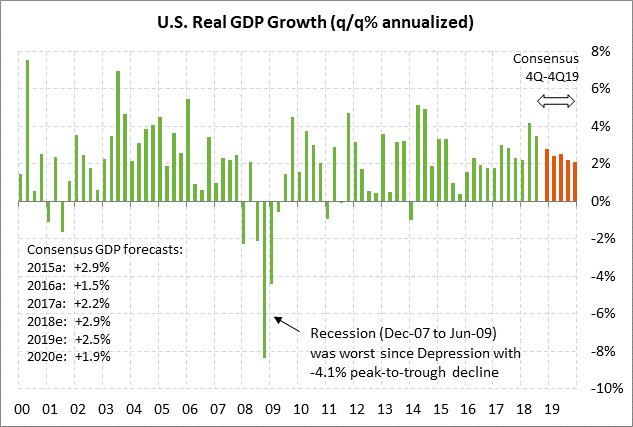

U.S. GDP expected to ease in coming quarters after no Q3 revision today — The consensus is for today’s Q3 GDP report to be unrevised at +3.5% (q/q annualized). Q3 personal consumption is expected to be revised slightly lower to +3.9% from +4.0%.

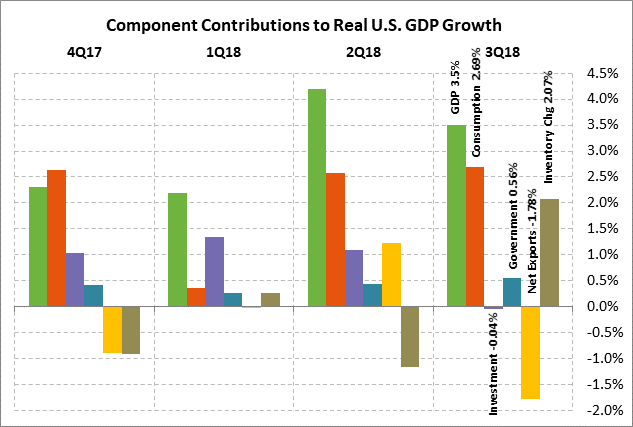

The Q3 GDP report of +3.5% looked very strong on its face. However, the increase was almost completely due to a strong 2.69 percentage point contribution from personal consumption. Inventories contributed a hefty 2.07 points but that was only a one-off contribution. On the weak side, government spending contributed a minor 0.56 points while investment subtracted -0.04 points and net exports subtracted a hefty -1.78 points.

U.S. GDP was very strong at +4.2% in Q2 and +3.5% in Q3. However, the market is now expecting GDP to ease to +2.6% in Q4 and +2.4% in Q1. The expected GDP rate near +2.5% in the new few quarters is still a strong figure and is well above the Fed’s estimate of long-term potential U.S. GDP growth of +1.8%. On a calendar year basis, the consensus is for GDP growth to be strong at +2.9% in 2018 but then fade to +2.6% in 2019 and +1.9% in 2020 as the effects of tax cuts fade and as higher interest rates bite.

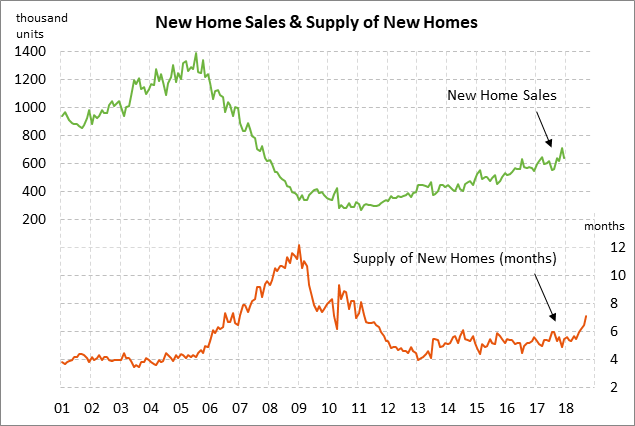

U.S. new home sales expected to snap 4-month losing streak — The market consensus is for today’s Oct new home sales report to show an increase of +4.0% to 575,000, reversing most of Sep’s -5.5% decline to 553,000. An increase today would snap the current 4-month losing streak of -15% to Sep’s 1-3/4 year low of 553,000 units. New home sales have fallen sharply in the past four months mainly because of higher mortgage rates and high home prices. The NAR’s U.S. housing affordability index fell to a 10-year low of 137.7 in June and then recovered only modestly to 146.7 in September.

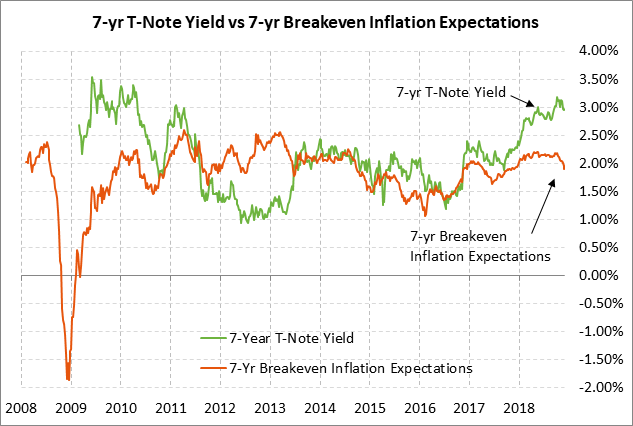

7-year T-note auction yield near 2-1/4 month low — The Treasury today will sell $18 bln of 2-year floating-rate notes and $32 bln of 7-year T-notes, concluding this week’s $129 billion T-note package. The $32 bln size of today’s 7-year T-note is up by $1 bln from October and by $4 bln from the $28 bln size that prevailed during 2016/17.

The 7-year T-note yield late yesterday afternoon was trading at 2.97%, which is near last week’s 2-1/4 month low of 2.94% and well below the early-Oct 8-1/2 year high of 3.20%. The 12-auction averages for the 7-year are as follows: 2.50 bid cover ratio, $17 million in non-competitive bids, 4.7 bp tail to the median yield, 33.1 bp tail to the low yield, and 44% taken at the high yield. The 7-year is of average popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 63.2% of the last twelve 7-year T-note auctions, which exactly matches the median of 63.2% for all recent Treasury coupon auctions.