- Powell’s dovish tone has much more bullish impact on stocks than on interest rate expectations

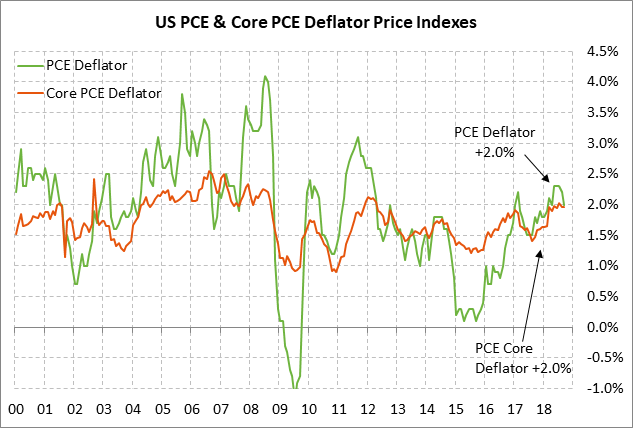

- Fed’s preferred inflation measure expected to remain near target

- U.S. personal income and spending expected to remain strong

- Pending home sales expected to show a small increase

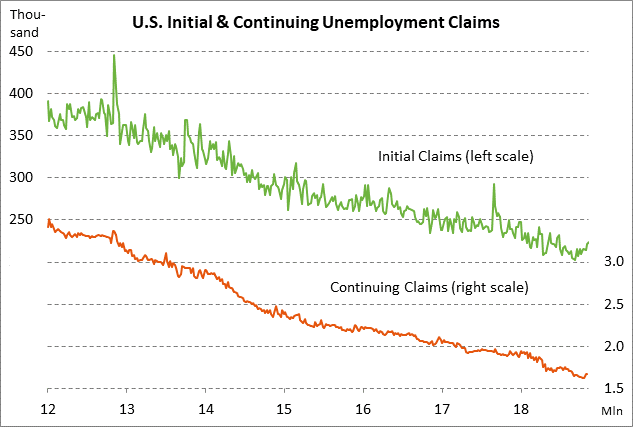

- Unemployment claims expected to remain favorable

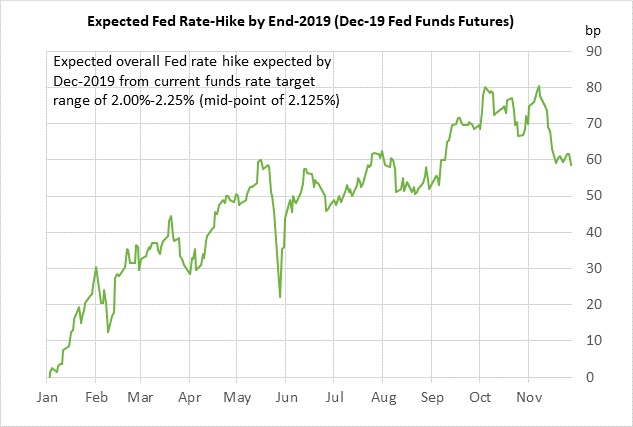

Powell’s dovish tone has much more bullish impact on stocks than on interest rate expectations — Fed Chair Powell’s dovish comments on Wednesday sparked a big +2.30% rally in the S&P 500 index but had only a relatively small 3-4 bp dovish impact on the back end of the federal funds futures curve.

The market reduced expectations for Fed rate-hikes through the end of 2019 by -3 bp to 58.5 bp, which translates to expectations of only +33.5 bp of rate hikes in 2019 after the expected +25 bp rate hike at the next FOMC meeting on Dec 18-19. There was no change in expectations of about 80% for a rate hike at the upcoming December FOMC meeting.

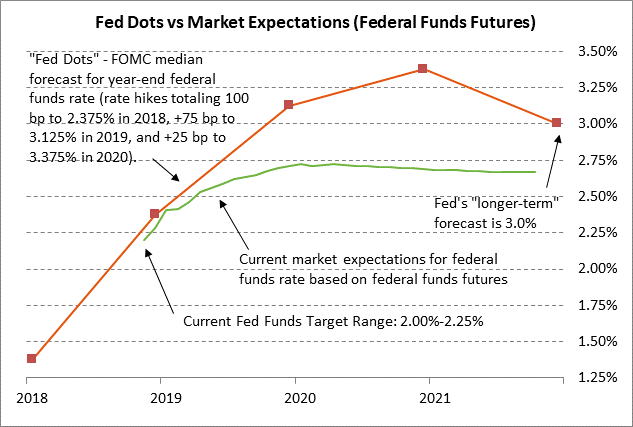

Mr. Powell said that interest rates remain “just below the broad range of estimates of the level that would be neutral for the economy.” His comment that interest rates are “just below” neutral was a big turnaround from his hawkish comments on Oct 3 when he said “we may go past neutral. But we’re a long way from neutral at this point, probably.” Mr. Powell on Wednesday also said there is no “preset policy path” and that decisions are data dependent. That raised hopes that the Fed after its expected December rate hike to 2.25%/2.50% will pause and perhaps delay further rate hikes.

The stock market rallied sharply on hopes that the FOMC will pause its rate-hike regime in 2019 as it waits for incoming data. The stock market also received a boost from other parts of Mr. Powell’s speech in which he said the Fed does not see broad-based excessive risk-taking or asset bubbles. He said that the Fed does not see “dangerous excesses” in the stock market and the valuations remain within normal ranges. Mr. Powell said the Fed’s main concern is with high corporate borrowing, although he said even that remains below historical peaks.

The dollar index on Wednesday fell sharply by -0.60% on Mr. Powell’s dovish comments as the dollar’s interest rate differential outlook for 2019 became a little less bullish for the dollar. The 2-year T-note yield fell by -2.4 bp to 2.809% while the 10-year T-note was little changed at 3.06%. T-note prices were supported by expectations for less Fed tightening in 2019, but were undercut by worries that the Fed might become complacent on inflation.

Today’s release of the minutes from the Nov 7-8 FOMC meeting will be rather anticlimactic after Fed Chair Powell yesterday essentially gave an update of the Fed’s latest thinking. The Nov 7-8 FOMC meeting was a nonevent in any case since the Fed left interest rates unchanged and made only minor changes in its post-meeting statement.

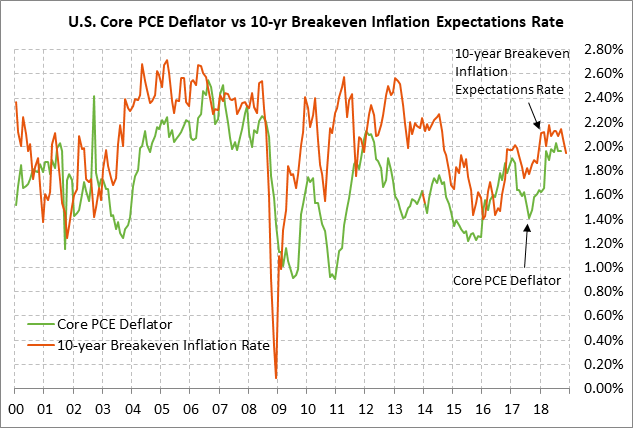

Fed’s preferred inflation measure expected to remain near target — The consensus is for today’s Oct PCE deflator to edge slightly higher to +2.1% y/y from Sep’s +2.0%, but the core deflator is expected to ease slightly to +1.9% from Oct’s +2.0%. The expected deflator report of +2.1% headline and +1.9% core would both be very close to the Fed’s +2.0% inflation target. The core deflator has been stuck at the 6-year high of +2.0% since May. The fact that the core deflator never rose above the Fed’s +2.0% target, and is now expected to dip to +1.9%, illustrates that the Fed is not under any pressure from an inflation standpoint to accelerate the pace of its rate hikes.

Indeed, the pressure on the Fed regarding inflation has eased substantially just in the past two months due to the -34% plunge in WTI oil prices. The 10-year breakeven inflation expectations rate in the past two months has dropped sharply by -22 bp to 1.95%. The 10-year breakeven rate actually fell to a 1-year low of 1.91% early Wednesday but then rebounded higher to 1.95% after Chairman Powell’s dovish comments revived some inflation concerns.

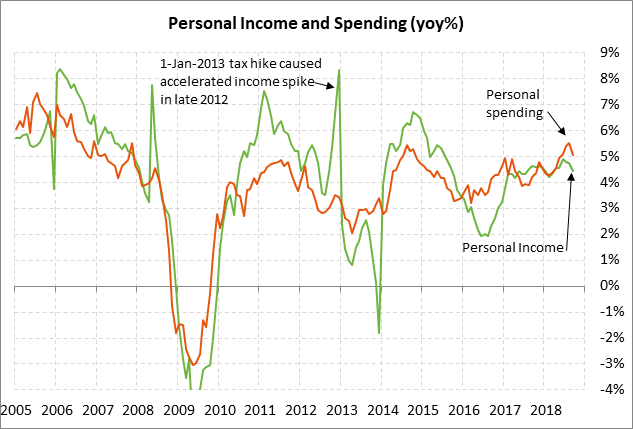

U.S. personal income and spending expected to remain strong — The consensus is for today’s Oct personal income and spending reports to both show an increase of +0.4% m/m, which would follow Sep’s respective reports of +0.2% and +0.4%. Personal income and spending remain strong and were up by +4.4% y/y and +5.0% y/y in September. Personal spending was by far the biggest contributor to GDP growth in the past two quarters. Personal spending contributed 2.57 percentage points to the Q2 GDP rate of +4.2% and 2.45 points to the Q3 GDP rate of +3.5%. U.S. income and spending continue to be supported by the Jan 1 tax cuts, the strong labor market, and strong consumer confidence.

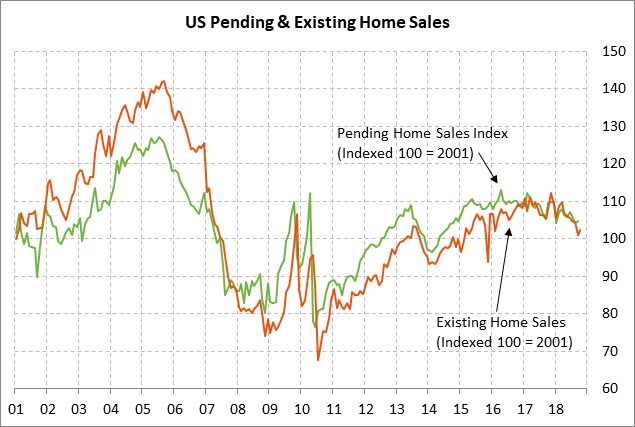

Pending home sales expected to show a small increase — The consensus is for today’s Oct pending home sales report to show an increase of +0.5% m/m, matching Sep’s increase. Pending home sales in Sep were underwater on a year-on-year basis at -3.4% y/y but are expected to improve to -2.8% y/y in today’s report for October.

The pending home sales report is a leading indicator for the existing home sales series since pending home sales contracts generally lead to closed home sales on a 1-2 month basis. U.S. existing home sales fell sharply by a total of -8.0% from April through September but snapped that decline in October with a small +1.4% increase. Homes sales have been hurt by a sharp drop in affordability caused by higher mortgage rates and the surge in home prices.

Unemployment claims expected to remain favorable — The consensus is for today’s initial claims report to show a small -4,000 decline (after last week’s +3,000) and for continuing claims to show a -5,000 decline to 1.663 million (after last week’s -2,000). Initial claims are only +22,000 above Sep’s 49-year low of 202,000 and continuing claims are only +38,000 above Oct’s 45-year low of 1.630 million.