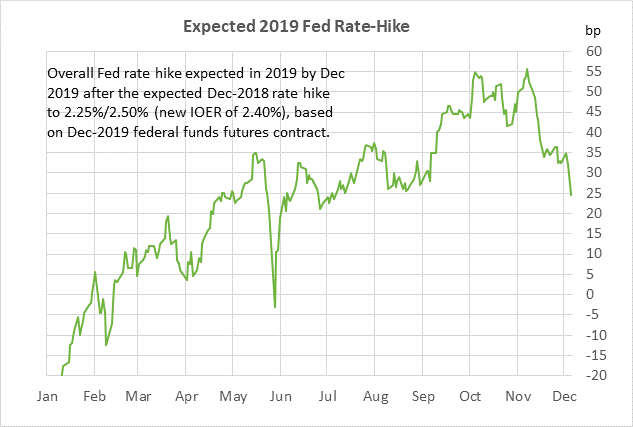

- Fed 2019 rate-hike expectations for below 25 bp due to stock market volatility and lower inflation expectations

- Congress punts government shutdown threat to Dec 21

- Stocks on guard for weaker-than-expected U.S. payroll report

- U.S. consumer sentiment expected to show its third monthly decline

- German CDU leadership vote could produce the next German Chancellor

Fed 2019 rate-hike expectations for below 25 bp due to stock market volatility and lower inflation expectations — Market expectations for Fed tightening have dropped sharply this week due to the sharp stock market sell-off and reduced inflation expectations tied in part to the plunge in oil prices.

The S&P 500 index on Thursday opened sharply lower on the news that Canada, at the behest of the U.S., arrested high-profile CFO Wanzhou Meng of Huawei Technologies, China’s largest smartphone and communications equipment manufacturer. The arrest outraged Chinese officials and could easily harden China’s trade position, potentially even ending the US/Chinese trade ceasefire before it gets started.

Stocks then staged an impressive recovery rally after dovish comments by two Fed officials and a WSJ report saying that Fed officials are considering “whether to signal a new wait-and-see mentality” after December’s rate hike. Dallas Fed President Kaplan on Thursday said he previously had a lot of confidence about higher interest rates but that “at this stage, you’re going to hear me be a lot more cautious and counsel patience.” Atlanta Fed President Bostic said, “I currently think we’re within shouting distance of neutral.”

Crude oil prices plunged -2.65% on Thursday as Russia dragged its feet on agreeing to a production cut and Saudi Arabia indicated that it would be satisfied with a 1 million bpd cut. A 1 million bpd production cut would be a step in the right direction but would not fully offset the 1.3 million bpd surplus that OPEC+ delegates mentioned last week, meaning global oil inventories would likely rise in 2019. OPEC+ at its meeting today is expected to make a final decision on its 2019 production cut. Due in part to continued weakness in oil prices, the 10-year breakeven inflation expectations rate on Thursday fell to a new 1-year low of 1.91%, down by -27 bp from 2.18% as recently as October.

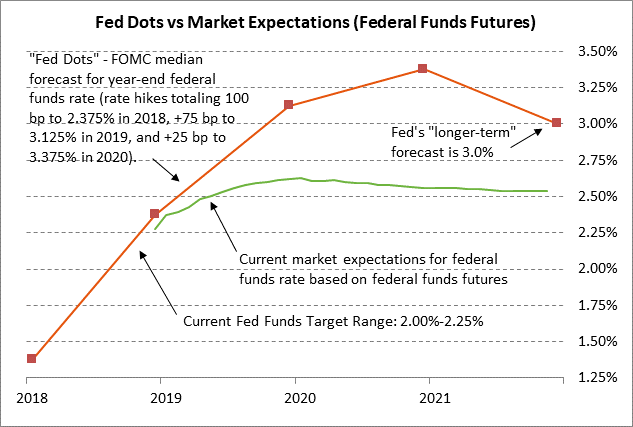

The markets this week have become convinced that the FOMC will hit the pause button after its expected rate hike in two weeks at the Dec 18-19 FOMC meeting. The market is still discounting a 100% chance of that December rate hike involving a +25 bp hike in the funds rate target range to 2.25%/2.50% and a +20 bp hike in the IOER (interest on excess reserves) rate to 2.40%. However, the market is now expecting only another +24.5 bp of rate hikes in 2019, down from +55.5 bp as recently as early-Nov. Moreover, the market is not fully discounting that +25 bp rate hike until Q4-2019.

Congress punts government shutdown threat to Dec 21 — Congress on Thursday approved a 2-week continuing resolution with a simple voice vote to keep the government funded through Dec 21, thus setting up midnight Dec 21 as the new potential shutdown time. President Trump has threatened to shut down the government if he doesn’t get at least $5 billion in border wall funding, whereas Senate Democrats are so far unwilling to go any higher than $1.6 billion. The markets are not particularly concerned about the showdown since a compromise is likely and since a shutdown in any case would involve only a few agencies of the government.

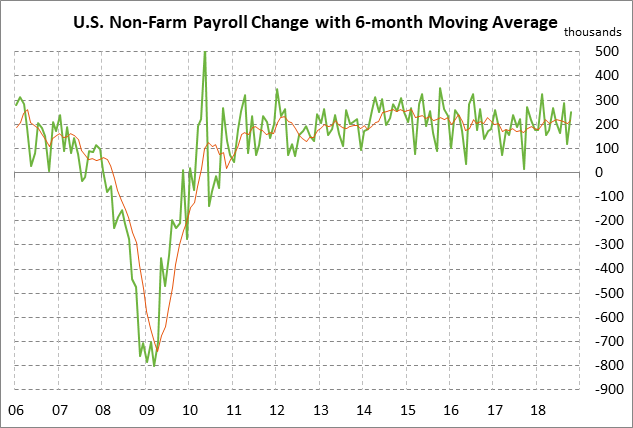

Stocks on guard for weaker-than-expected U.S. payroll report — The consensus is for another solid payroll report today of +198,000, which would be just mildly below the 12-month trend average of +210,000 and down from Oct’s very strong report of +250,000. The stock market is likely to react negatively if today’s payroll report is weaker-than-expected. Any weak economic data would exacerbate this week’s concern that a nearly-inverted yield curve might be signaling a recession. Yesterday’s Nov ADP report of +179,000 was mildly below the consensus of +195,000.

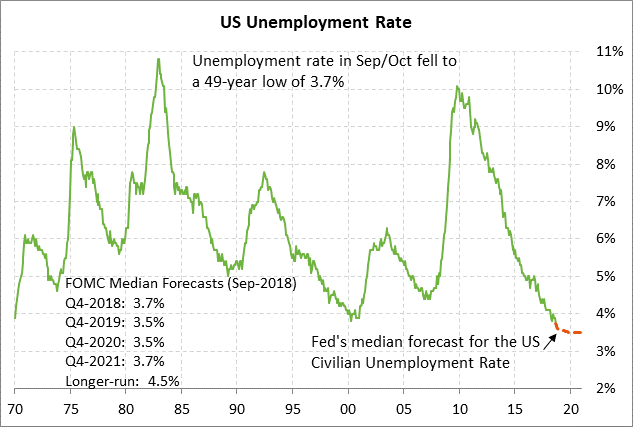

The consensus is for today’s Nov unemployment rate to be unchanged from the 49-year low of 3.7% seen in Sep-Oct. The unemployment rate has already fallen to the 3.7% level that the FOMC has been forecasting for the end of this year. The FOMC is forecasting that the unemployment rate will fall another -0.2 points to 3.5% in 2019 and then remain at that level in 2020. The current unemployment rate of 3.7% is well below the FOMC’s estimate of a long-run natural unemployment rate of 4.5%, illustrating the current tightness of the U.S. labor market.

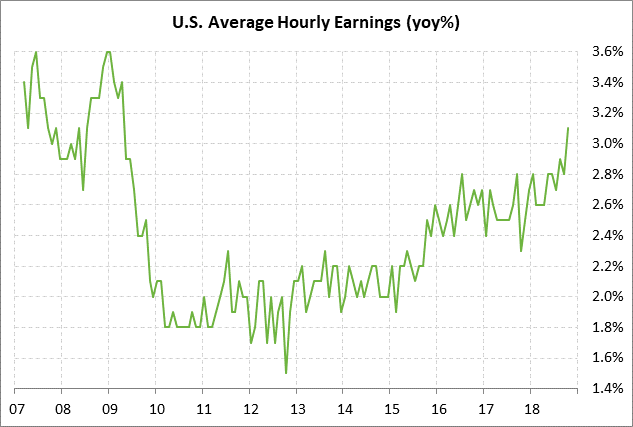

The markets are waiting to see if the tight labor market pushes wages any higher, which would of course be a negative development for the inflation outlook and for corporate profits. The consensus is for today’s Nov average hourly earnings report to be unchanged from October’s +3.1% y/y. The breakout in hourly earnings in October to a new 9-1/2 year high of +3.1% was a bit alarming after wages in the previous two years remained steady in the narrow range of +2.4%/2.8%.

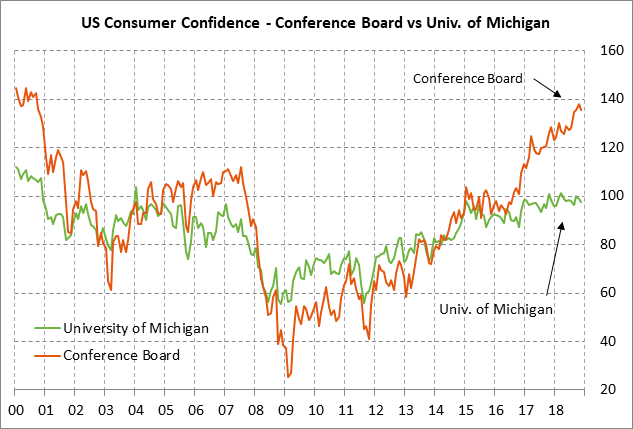

U.S. consumer sentiment expected to show its third monthly decline — The market consensus is for today’s preliminary-Dec University of Michigan U.S. consumer sentiment index to show a small decline of -0.5 to 97.0, adding to Nov’s decline of -1.1 to 97.5. The index as recently as September rose to an 8-month high of 100.1 where it was only 0.3 points below March’s 15-year high of 101.4. However, the index in Oct-Nov then fell by a combined -2.6 points and another decline is expected today.

U.S. consumer confidence in general remains strong due to (1) the strong economy and labor market, (2) rising wages and income, (3) the Jan 1 tax cuts, and (4) falling gasoline prices. However, consumers might be starting to get cold feet due to (1) the Fed’s steady rate-hike regime, (2) the US/Chinese trade war, (3) Washington political uncertainty, and (4) the downward correction in the stock market.

German CDU leadership vote could produce the next German Chancellor — The Christian Democratic Union holds a 2-day party conference today and tomorrow to choose a new leader to succeed Angela Merkel. The new CDU leader could become the next Chancellor after Angela Merkel steps down as Chancellor after the next national election, assuming the CDU fares well enough in the next election. The CDU leadership showdown is mainly between Ms. Merkel’s hand-picked successor, CDU general secretary Annegret Kramp-Karrenbauer, and business executive and Merkel-rival Friedrich Merz.