- FOMC expected to turn more dovish in its guidance

- Hire-wire US/Chinese trade talks begin Wednesday

- Prime Minister May presses ahead with today’s key Brexit votes

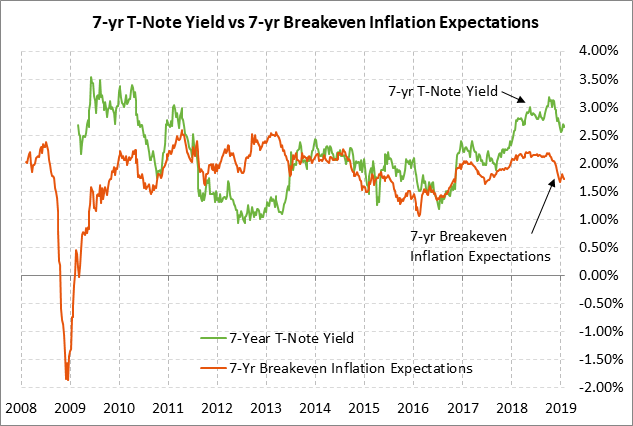

- 7-year T-note auction to yield near 2.65%

- U.S. home prices expected to show another solid gain

- US consumer confidence expected to fall

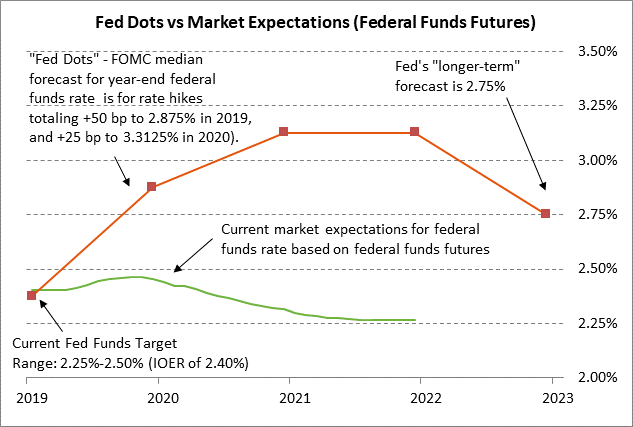

FOMC expected to turn more dovish in its guidance — The FOMC at its 2-day meeting that begins today is expected to turn more dovish and indicate more clearly that policy is on hold while it waits for more certainty on the macroeconomic outlook. However, that dovish tone will have to be relayed in the post-meeting statement and by Fed Chair Powell in his post-meeting press conference since there will be no new Fed forecasts and no new Fed-dots at this week’s meeting.

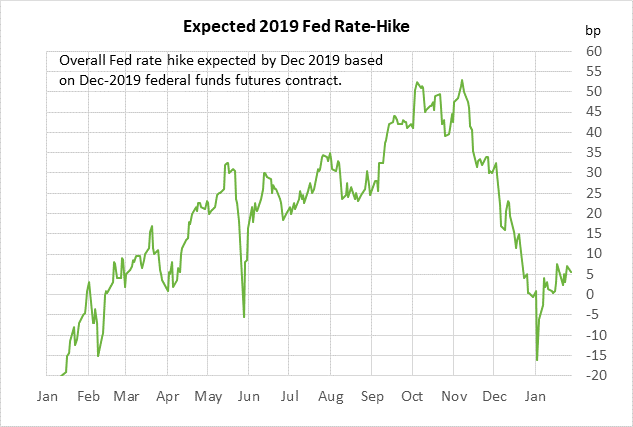

The market is discounting a zero chance for a Fed rate hike at this week’s meeting. The February 2019 federal funds future contract is trading at 2.40%, which means the market is expecting the funds rate to average 2.40% in February, exactly matching its current trading level.

Looking ahead, the market is currently discounting a 24% chance for a +25 bp rate hike by later this year. The December 2019 federal funds contract is trading at 2.46%, which is +6 bp above the current level and translates to a rate-hike probability of 24% (i.e., 6/25). The December 2020 federal funds futures contract is trading at 2.32%, which is down by -8 bp from the current level of 2.40%.

Hire-wire US/Chinese trade talks begin Wednesday — The 2-day talks led by Chinese Vice Premier Liu He (Chinese President Xi’s top economic advisor) and USTR Lighthizer talks will begin on Wednesday. The talks will be critical as to whether there will be a US/Chinese trade agreement, or at least enough progress for President Trump to extend the March 1 deadline. There will apparently be some mid-level US/Chinese trade talks today after reports that at least two mid-level Chinese officials arrived in Washington on Monday.

The Wall Street Journal late Monday reported that China this week will offer a big increase in Chinese purchases of U.S. farm and energy products but will offer only modest reforms in industrial policies. The WSJ said that China will fight U.S. demands for deep structural changes on IP and state-subsidies. The question is whether the Chinese offer for structural changes will be enough to satisfy President Trump and USTR Lighthizer.

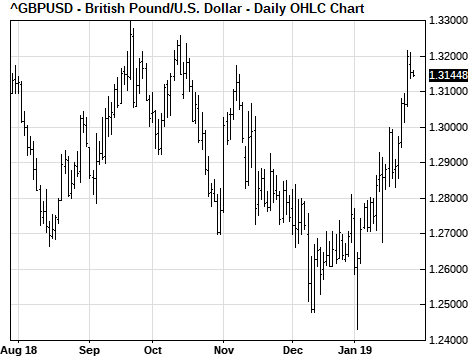

Prime Minister May presses ahead with today’s key Brexit votes — Sterling on Monday fell back from last Friday’s 3-1/2 month high but remains in generally strong shape so far since the betting odds indicate a low probability of 25% for a no-deal Brexit on March 29. Sterling has rallied in the past three weeks since the market has become convinced of the low chances for a no-deal Brexit, either through a last-minute agreement or, more likely, through a delay in the March 29 deadline. A no-deal Brexit would likely be a disaster since there would suddenly be a hard customs border with massive import/export product delays and a jump in tariffs to WTO default levels.

The UK Parliament today is scheduled to vote on Prime Minister May’s Plan B separation agreement as well as a number of amendments. The Speaker of the Parliament has not yet decided exactly which amendments will be put up for a vote, making the outcome of Tuesday’s vote highly uncertain.

Prime Minister May is reportedly supporting an amendment by Murrison-Brady that would essentially scrap the Irish border backstop by saying that the backstop should be replaced with “alternative arrangements.” If that passes Parliament, then Ms. May could go to the EU and demand a softening of the EU’s Irish backstop, which was the main provision that caused her plan to go down to an epic defeat in the recent vote in Parliament. The EU has so far adamantly refused to soften its Irish border backstop.

The other major amendment that may be considered is the Cooper-Boles amendment that would prevent a no-deal Brexit by delaying the Brexit deadline if there is no separation agreement by March 29. Ms. May is trying to sidestep that amendment by promising that Parliament will get another vote to prevent a no-deal Brexit if she cannot get the EU to change the Irish border backstop in time for a separation agreement by March 29.

7-year T-note auction to yield near 2.65% — The Treasury today will auction $20 billion of 2-year floating rate notes and $32 billion of 7-year T-notes. Today’s 7-year T-note issue was trading at 2.65% in when-issued trading late yesterday afternoon. The 7-year T-note yield has rebounded higher by +23 bp from the early-Jan 1-year low of 2.42% mainly because of January’s recovery in the U.S. stock market. The 12-auction averages for the 7-year are: 2.52 bid cover ratio, $18 million in non-competitive bids, 4.4 bp tail to the median yield, 35.3 bp tail to the low yield, 28% taken at the high yield, and 67.4% taken by foreign/indirect bidders (well above the recent coupon average of 62.8%).

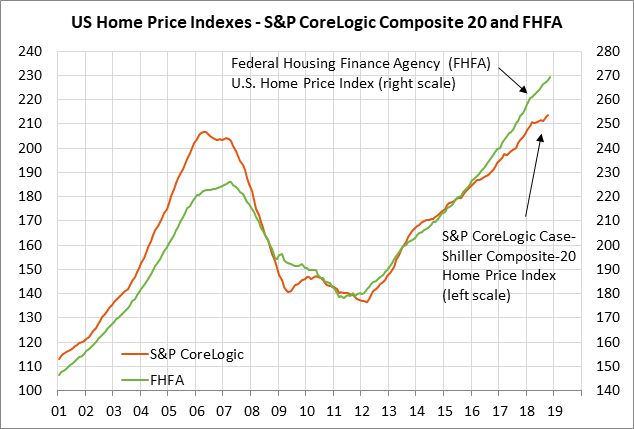

U.S. home prices expected to show another solid gain — The consensus is for today’s Nov S&P CoreLogic composite-20 home price index to show an increase of +0.4% m/m and +4.9% y/y, which would be little changed from October’s report of +0.4% m/m and +5.0% y/y. Home prices are expected to move higher despite the recent lull in home sales caused by last year’s rise in mortgage rates and poor home affordability.

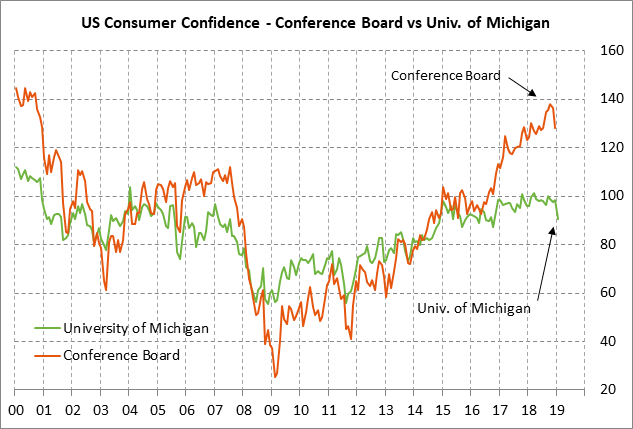

US consumer confidence expected to fall — The consensus is for today’s Jan Conference Board U.S. consumer confidence index to show a -4.1 point decline to 124.0, adding to December’s sharp -8.3 point decline to 128.1. U.S. consumer confidence has recent taken a hit due to the Oct-Dec stock market correction and the Dec/Jan U.S. government shutdown. The University of Michigan’s preliminary-Jan U.S. consumer sentiment index has already been released and showed a -7.6 point decline, which did not bode well for today’s Conference Board report.