- FOMC expected to adjust guidance to allow for pause

- Crunch time for US/Chinese trade talks

- Parliament tries last-ditch effort on Irish backstop

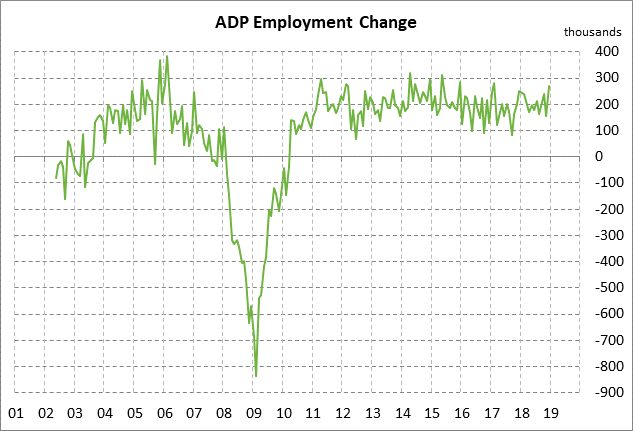

- ADP employment expected to moderate

-

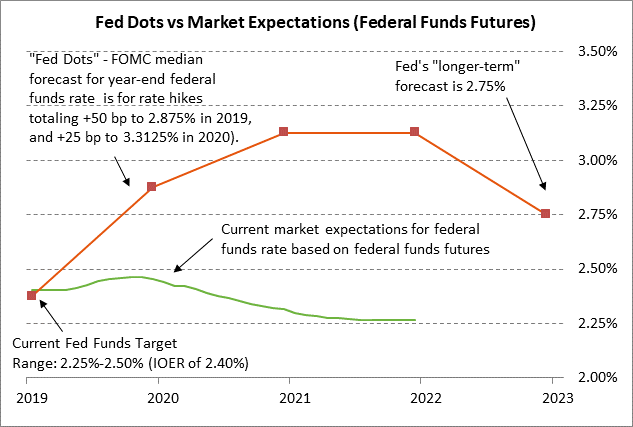

FOMC expected to adjust guidance to allow for pause — The FOMC at its 2-day meeting that ends today is expected to turn more dovish and indicate that it is willing to be patient while it waits for more certainty on the macroeconomic outlook. However, the FOMC is likely to indicate that it still intends to raise the funds rate eventually so that it at least reaches the Fed’s perceived long-term neutral rate of 2.75%. The Fed at today’s meeting will not update the Fed-dot forecasts, which in December called for two rate hikes in 2019 and a third rate hike in 2020.

While the federal funds futures market is indicating only a minor 18% chance of a rate hike in 2019, a recent Bloomberg survey found that U.S. economists are still predicting two rate hikes later this year. Two more rate hikes would push the funds rate up from its current level of 2.25-2.50% to 2.75%-3.00%, which would be in line with the Fed’s long-term neutral rate. The market is discounting a zero chance for a Fed rate hike at today’s meeting.

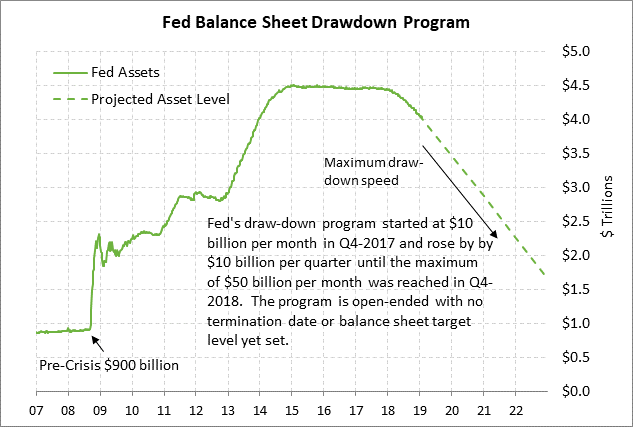

The FOMC at this week’s meeting is expected to begin actively discussing the future of its balance sheet. The FOMC may not say much about the balance sheet today, but the Fed needs to start communicating with the markets in a more organized way about its balance sheet plans. Fed Chair Powell caused a big sell-off in stocks after December’s FOMC meeting when he said that the Fed’s balance sheet drawdown program is on “auto-pilot.” Mr. Powell later added that the future balance sheet “will be substantially smaller than it is now.” After being browbeaten by the markets over his hawkish balance sheet comments, Mr. Powell finally softened up a bit by saying that the Fed could curb its balance sheet drawdown program if it becomes necessary.

The markets are chomping at the bit to know how much longer the Fed’s balance sheet reduction program will last because the program was cited as one the reasons for the sharp downside stock market correction seen late last year. The FOMC has not yet specified an ending date for the program or a final resting place for the level of the balance sheet.

The eventual target for the balance sheet depends in part on the larger issue of whether the Fed in the future will use a floor or corridor system for running monetary policy. A recent survey of government securities dealers by the NY Fed found a consensus that the program would end with the balance sheet at $3.5 trillion, which implies the program could end as soon as early 2020.

Crunch time for US/Chinese trade talks — The 2-day trade talks begin today led by Chinese Vice Premier Liu He (Chinese President Xi’s top economic advisor) and USTR Lighthizer. This week’s high-level talks will be critical as to whether there will be a US/Chinese trade agreement, or at least enough progress for President Trump to extend the March 1 deadline.

The Wall Street Journal late Monday reported that China this week will offer a big increase in Chinese purchases of U.S. farm and energy products but will offer only modest reforms in industrial policies. The WSJ said that China will fight U.S. demands for deep structural changes on IP and state-subsidies.

The question is whether the Chinese offer for structural changes will be enough to satisfy President Trump and USTR Lighthizer, or whether Mr. Trump decides to raise tariffs on March 1 to try to soften up the Chinese position on structural changes during another round of negotiations later this year. On the more hopeful side, Mr. Trump now seems to recognize that a strong U.S. stock market going into next year’s election campaign depends in large part on a resolution of US/Chinese trade tensions.

Parliament tries last-ditch effort on Irish backstop — The UK Parliament on Tuesday voted to take a higher-risk path for Brexit by adopting an amendment that calls for the EU’s Irish border backstop to be scrapped by using the non-meaningful phrase of “alternative arrangements.” The odds are low that the EU will agree to that fudge, which means that the UK will be left without a Brexit separation agreement that is acceptable to both the UK Parliament and the EU with just 8 weeks left until the March 29 Brexit deadline.

Meanwhile, Parliament on Tuesday narrowly rejected the Cooper amendment by a vote of 321-298 that would have ruled out a no-deal Brexit on March 29 by requesting a deadline extension if a Brexit separation agreement could not be reached in time. The good news on that issue, however, was that a near-majority of 298 members of Parliament voted against a no-deal Brexit and that Prime Minister May is reportedly now telling colleagues that she will not allow a no-deal Brexit.

Ms. May will now head to Brussels to see if she can browbeat the EU into relenting on the Irish border backstop. After she fails, as seems assured, Ms. May will have no choice but to request a delay in the March 29 Brexit deadline to provide time to develop a new strategy.

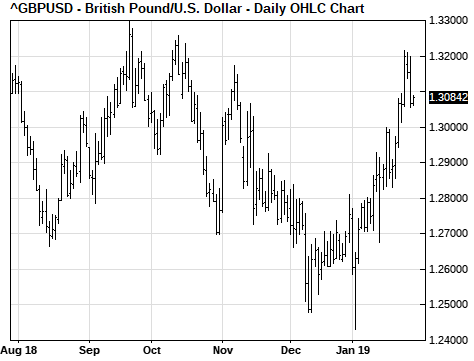

Sterling on Tuesday continued to fall back from last Friday’s 3-1/2 month high and closed the day down -0.74% after Parliament’s votes. However, sterling remains in generally favorable shape since Parliament made it fairly clear that it will not allow a no-deal Brexit on March 29, which is the main thing the markets are currently worried about.

ADP employment expected to moderate — The consensus is for today’s Jan ADP employment report to show an increase of +183,000, down from Dec’s +271,000 and below the 12-month trend average of +209,000. The consensus is for Friday’s payroll report to show an increase of +165,000, down from Dec’s strong report of +312,000.