- 10-year T-note yield direction likely turns on outcome of US/Chinese trade talks

- 10-year T-note auction size stabilizes

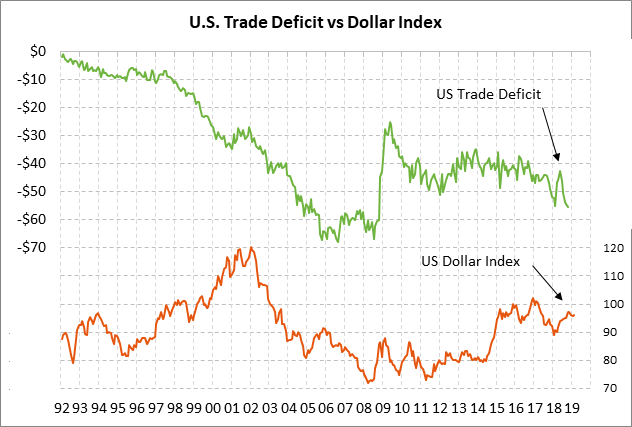

- U.S. trade deficit expected to narrow from Oct’s 10-year high

- EIA report

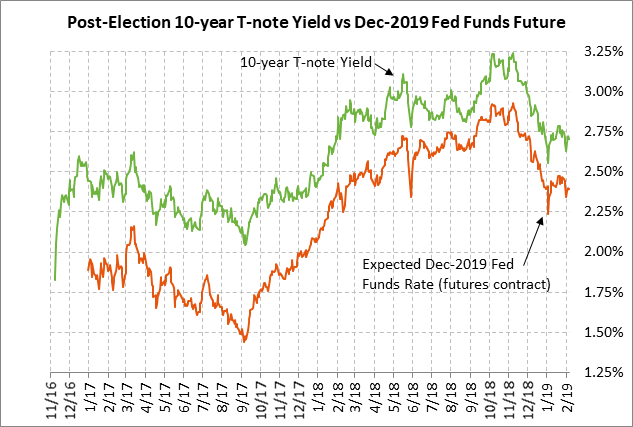

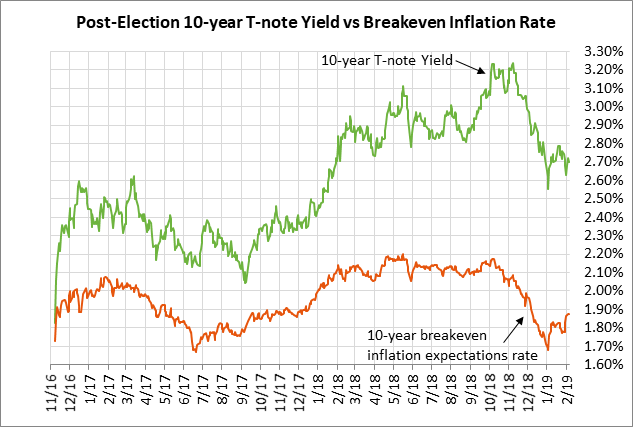

10-year T-note yield direction likely turns on outcome of US/Chinese trade talks — The 10-year T-note yield has fallen sharply by -56 bp from last October’s 7-3/4 year high of 3.26% to the current level of 2.70%.

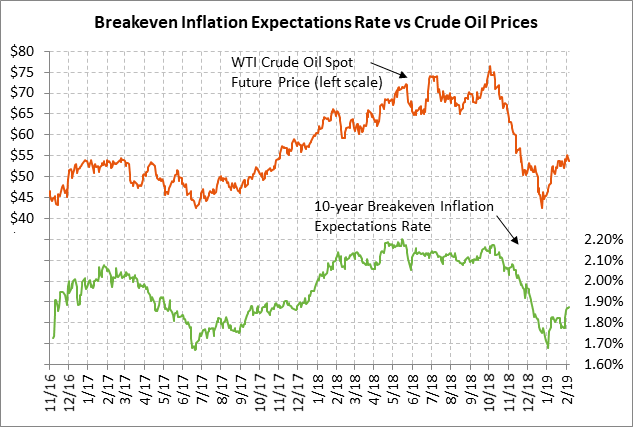

Bullish factors for T-note prices that led to the Oct/Jan T-note yield decline include (1) the Fed’s pause in its interest-rate hike regime and market expectations that the next Fed move could be a rate cut in 2020, (2) the sharp drop in the 10-year breakeven inflation expectations rate caused mainly by the -45% plunge in crude oil prices seen in Q4-2018, (3) expectations for slower U.S. GDP growth in 2019 and concern about the slowing Chinese economy, (4) the sharp downside global stock market correction seen in Q4-2018 although U.S. stocks have since regained nearly two-thirds of that decline, and (5) safe-haven demand tied to the stock market volatility, US/Chinese trade tensions, Washington political strife (including the 35-day partial U.S. government shutdown), and Brexit.

The Fed’s dovish turn is a key factor behind the decline in the 10-year T-note yield. The FOMC as recently as its December meeting raised its funds rate target by +25 bp to 2.25%/2.50% and adopted a median Fed-dot forecast for two rate hikes in 2019 and a third rate hike in 2020, which would put the funds rate target at 3.00%/3.25% by the end of 2020. However, the Q4 stock market correction and the slowing Chinese economy finally convinced the Fed that it was being overly hawkish. The FOMC at its meeting last week surprised the market by announcing a fully-neutral interest rate guidance and dropping its reference to slowly raising interest rates.

The 10-year T-note yield has also been able to fall in the past several months because of the sharp -33 bp decline in the 10-year breakeven inflation expectations rate from last May’s 4-1/2 year high of 2.21% to the current level of 1.88%. The 10-year breakeven rate has been able to fall because of (1) the 45% plunge in oil prices seen in Q4, (2) slower global economic growth and product demand, and (3) tepid inflation statistics with the Oct core PCE deflator at +1.9% y/y.

The near-term outlook for the T-note market depends heavily on the U.S. and Chinese economies and whether there is a resolution of US/Chinese trade tensions. If President Trump goes ahead with his threat to raise penalty tariffs to 25% from 10% on $200 billion of Chinese products on March 1, then the 10-year T-note yield is likely to see a renewed decline as the markets look forward to even weaker growth in China. China has built up a massive quantity of household and corporate debt in the past decade and further weakness in the Chinese economy could even lead to a debt and banking crisis.

Alternatively, if US/Chinese trade tensions are resolved and the Chinese economy can stabilize, and if U.S. GDP growth remains near or above 2.5%, then the U.S. T-note yield is likely to move moderately higher. In our view, the Fed still wants to raise its funds rate by about another 50 bp and will look for the opportunity to make that move if the global economy revives and inflation starts moving higher.

The most likely scenario is probably somewhere in the middle where US/Chinese trade tensions remain in a slow boil and the Chinese economy continues to slow this year. The U.S. economy is also likely to slow this year due to weak European growth, slower Chinese growth, and the fading stimulus from the 2018 tax cut. That scenario suggests sideways to mildly lower T-note yields this year.

10-year T-note auction size stabilizes — The Treasury today will sell $27 billion of new 10-year T-notes. The Treasury will then conclude this week’s $84 bln refunding operation by selling $19 bln of new 30-year T-bonds on Thursday. The Treasury at this week’s refunding operation finally stopped raising the size of its 10-year refunding auction at $27 billion, up from $23 billion as recently as late-2017.

The 12-auction averages for the 10-year are: 2.50 bid cover ratio, $22 million in non-competitive bids, 4.5 bp tail to the median yield, 24.2 bp tail to the low yield, and 63% taken at the high yield. The 10-year is mildly above average in popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 62.8% of the last twelve 10-year T-note auctions, mildly above the median of 61.9% for all recent coupon auctions.

U.S. trade deficit expected to narrow from Oct’s 10-year high — The market consensus is for today’s Nov trade deficit to narrow modestly to -$54.0 billion from October’s 10-year high -$55.5 billion. The U.S. trade deficit has widened mainly because export growth of +6.3% y/y has lagged behind import growth of +8.5% y/y. U.S. exports have been hurt by retaliatory tariffs while imports have held up relatively well (despite U.S. tariffs) because of the strong U.S. economy. The wide U.S. trade deficit continues to be a mildly bearish long-term factor for the dollar.

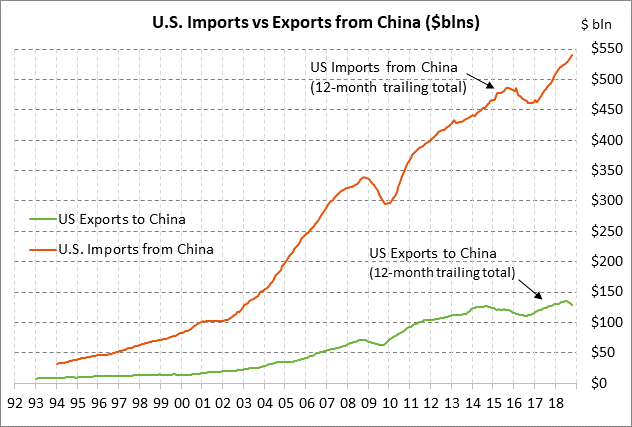

Meanwhile, the US/Chinese trade deficit in October rose to a record high of $43.102 billion, producing a 12-month cumulative deficit of a record -$410.7 billion. U.S. imports to China in the 12-months through October of $540 billion swamped U.S. exports of $129 billion, leading to the record deficit. USTR Lighthizer and Treasury Secretary Mnuchin will travel to China next week for a new round of high-level US/Chinese trade talks, according to Bloomberg.

EIA report — The consensus for today’s weekly EIA report is for a 1.5 mln bbl rise in both crude oil and gasoline inventories, and -2.0 mln bbl decline in distillate inventories.