- Weekly global market focus

- Trade tensions will remain in the news this week

- Brexit news will return this week

- Big earnings week

- U.S. home sales expected to give back some of Feb’s surge

Weekly global market focus — The U.S. markets this week will focus on (1) any trade news as US/Japanese trade talks resume late this week and as the markets await confirmation that US/Chinese face-to-face talks will resume next week, (2) a big week of Q1 earnings reports with 154 of the S&P 500 companies reporting, (3) the Treasury’s sale this week of $133 billion of T-notes, and (4) June crude oil prices, which are trading just below the recent 5-3/4 month nearest-futures high of $64.79.

This week’s U.S. economic calendar is fairly busy with several housing reports and Friday’s Q1 GDP report (expected +2.2%) and final-April U.S. consumer sentiment index (expected +0.1 to 97.0 after the prelim-April -1.5 to 96.9).

On the Washington politics front, House Democrats today will hold a private conference call in which the topic of impeachment may come up. House Democratic leaders are downplaying the possibility of impeachment following last Thursday’s release of the Mueller report but there is pressure from some in the Democratic party to proceed with an impeachment inquiry, which would increase Washington political uncertainty and be potentially bearish for the U.S. stock market. Separately, there are reports that former VP Joe Biden may announce his candidacy for the presidency as soon as this Wednesday, which could change the complexion of the 2020 presidential race.

The Bank of Canada at its policy meeting on Wednesday is expected to leave its policy unchanged with its benchmark overnight interest rate at 1.75%.

In Europe, the markets are closed today for the Easter Monday holiday. The ECB will release its monthly economic bulletin on Wednesday. There several European confidence reports this week including Tuesday’s April Eurozone consumer confidence index (expected +0.2 to -7.0 after March’s +0.2 to -7.2), Wednesday’s French April business confidence (expected unch at 105) and German April IFO business climate index (expected +0.3 to 99.9), and Friday’s French April consumer confidence index (expected +1 to 97).

In Asia, the markets will focus on any US/Chinese trade-talk news and on two summits with Russian President Putin meeting with Chinese President Xi in Beijing and with Japanese Prime Minister Abe meeting with President Trump in Washington. The Bank of Japan at its meeting on Wed/Thu is unanimously expected to leave its monetary policy unchanged.

Trade tensions will remain in the news this week — The markets this week will watch for confirmation of last week’s media reports that Lighthizer/Mnuchin will travel to China for another round of face-to-face trade talks next week (April 29) and that Chinese Vice Premier Liu will travel to Washington for talks the following week (May 6). Bloomberg reported that the Trump administration wants to announce a final trade agreement during Mr. Liu’s visit to Washington in the week of May 6 and a date in late May for a Trump/Xi signing summit.

On the Japanese trade front, Japanese Trade Minister Motegi said last week, after his talks with USTR Lighthizer, that he expects to return to the U.S. this week for another round of talks. Mr. Motegi may accompany Japanese Prime Minister Abe who will be in Washington later this week for a summit with President Trump. As part of the US/Japanese summit talks, Japanese Finance Minister Aso is expected to meet with Treasury Secretary Mnuchin to discuss U.S. demands for a currency agreement.

On the European trade front, the markets are waiting for news on when US/EU trade talks will begin. The EU last week finally gave EU Trade Commissions Malmstrom the mandate she needs to begin the talks.

Brexit news will return this week — Brexit will be back in the news this week after the UK Parliament returns from its Easter recess. Prime Minister May is under heavy pressure to get her Brexit withdrawal approved by Parliament in time to cancel the UK elections for members of the European Parliament on May 23, which would be politically damaging for the Conservative Party. However, the good news is that there cannot be a no-deal Brexit until at least the current Brexit deadline of October 31.

Ms. May’s negotiations with the Labour Party are reportedly going slowly. The only way for Ms. May to get a Brexit agreement through Parliament appears to be with help from the Labour Party, although that would cause an uproar among the hardline Brexiteers in the Conservative Party since Ms. May would likely to be forced to agree to the Labour Party demand that the UK would remain in the EU customs union.

Meanwhile, backbench Conservative MPs this week will be plotting to eject Ms. May as party leader by changing the rules and shortening the requirement that the party cannot vote on ejecting Ms. May as party leader for 1-year from the last challenge. The 1922 committee of backbench Conservative MPs plans to meet this week to discuss a potential rule change that could allow them to oust Ms. May by late June, shortly after the May 23 European elections, according to the Sunday Times.

Big earnings week — This is a big earnings week with 154 of the S&P 500 companies due to report. The consensus is for SPX Q1 earnings growth of -1.7% y/y, according to Refinitiv. The consensus is for annual earnings growth of +2.9% in 2019 and +12.0% in 2020.

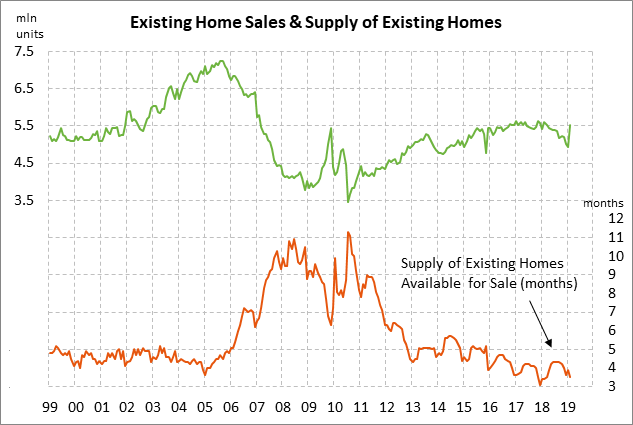

U.S. home sales expected to give back some of Feb’s surge — Today’s Mar U.S. existing home sales report is expected to show a -3.8% decline to 5.30 million, falling back after Feb’s +11.8% surge to a 1-year high of 5.51 million.