- Inflation expectations rise as oil prices surge on halt to Iranian oil waivers

- U.S. new home sales expected to show a modest decline but remain generally strong

- U.S. home prices expected to show another sharp rise

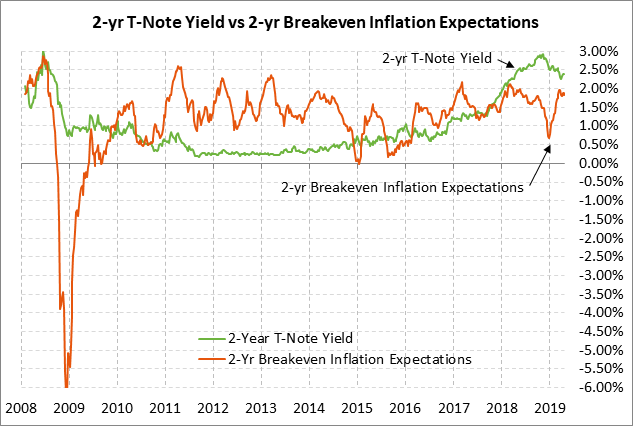

- 2-year T-note auction to yield near 2.39%

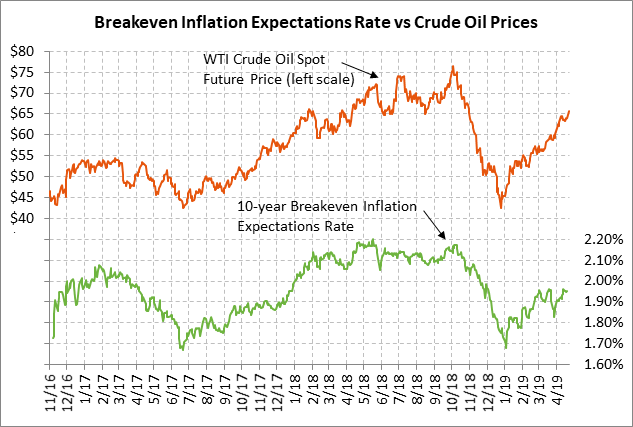

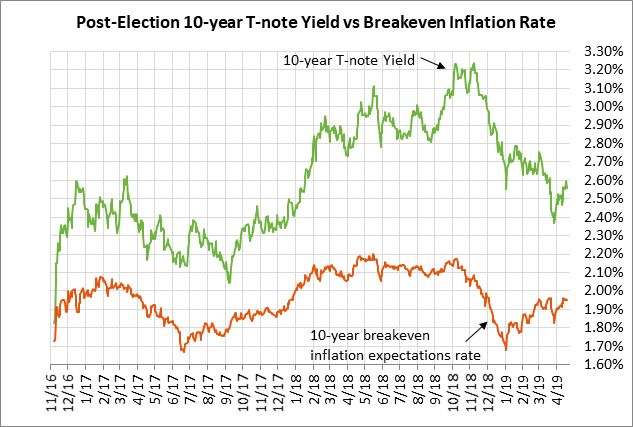

Inflation expectations rise as oil prices surge on halt to Iranian oil waivers — The 10-year breakeven inflation expectations rate on Monday rose by +0.4 bp to 1.955%, which is just 2 bp below March’s 4-3/4 month high of 1.974%. The 10-year breakeven rate shows a fairly strong correlation with oil prices and has risen by +14 bp since late March as June WTI oil prices rallied by $6.75 per barrel (+11%) to the current level of 65.76. The higher 10-year breakeven rate has been a factor behind the recent +22 bp rise in the 10-year T-note yield, along with less dovish Fed expectations.

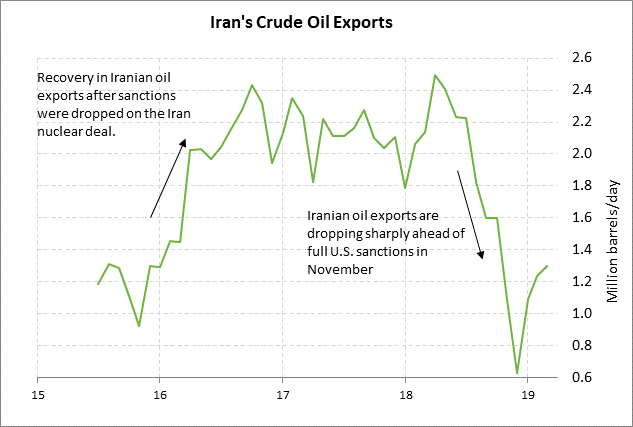

June Brent oil prices rallied by +2.9% on Monday after the Trump administration surprised the markets by announcing that there will be no renewal of the sanction waivers that expire on May 2 for buying Iranian crude oil. Iran exported about 1.3 million bpd of crude oil in March, meaning that as of May 2, world oil supplies could drop by as much as 1.3 million bpd. However, China may continue to buy Iranian oil despite the U.S. threat of sanctions, meaning Iranian oil exports may not go to zero. In March, China was Iran’s biggest customer, buying 613,000 bpd of Iranian oil.

The Trump administration on Monday sought to temper the rally in oil prices on its waiver announcement by saying that it had received commitments from Saudi Arabia and the UAE to boost production to offset the drop in Iranian oil exports. Saudi Arabia has the capacity to boost production by some 1 million bpd on short notice and the UAE has the capacity to boost production by about 500,000 bpd.

Saudi Arabia’s Oil Minister Khalid Al-Falih on Monday said that Saudi Arabia will ensure that adequate oil supplies are available and that the oil market “does not go out of balance.” However, Saudi Arabia will likely go slow on boosting production considering how it was burned last year. Saudi Arabia last year boosted production to offset the Trump administration’s reinstatement of Iran sanctions, only to find out later that the U.S. decided to allow waivers for up to 1.25 million bpd of Iranian oil, meaning Iranian oil exports would not fall by as much as originally thought.

Iran on Monday responded to the U.S. announcement of its plan to drive Iranian oil exports to zero by saying that it will close the Strait of Hormuz if it is unable to export any oil. Iran in past years has periodically threatened to close the Strait of Hormuz through which passes 20% of the world’s oil exports. Any attempt by Iran to close the Strait of Hormuz could easily draw military action by the U.S. and could even result in an all-out U.S.-Iranian war.

The news of the end of Iranian oil waivers was more bullish for Brent crude than it was for U.S. WTI crude since Brent crude is the benchmark for world crude oil whereas U.S.-based WTI crude prices are being held down in part by near-record U.S. oil production. June Brent on Monday closed +2.07 (+2.88%) at $74.04 per barrel, while June WTI crude closed +1.48 (+2.31%) at $65.55. The premium of June Brent crude oil futures over June WTI futures widened to a 5-week high of $8.49 on Monday.

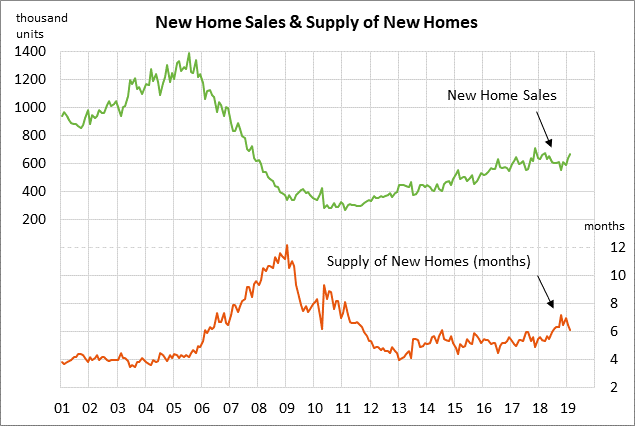

U.S. new home sales expected to show a modest decline but remain generally strong — The consensus is for today’s March new home sales report to show a decline of -3.0% to 647,000, reversing part of Feb’s +4.9% increase to 667,000. New home sales in February were in strong shape at only -6% below the 11-year high of 712,000 posted in November 2017. New home sales rose sharply by a total of +13.1% in Jan-Feb thanks mainly to the sharp decline in mortgage rates seen since the Fed gave up its rate-hike regime and switched to a neutral policy. The 30-year mortgage rate is currently at 4.17%, up by +9 bp from the late-March 15-month low of 4.08%, but down sharply by -77 bp from last November’s 8-year high of 4.94%.

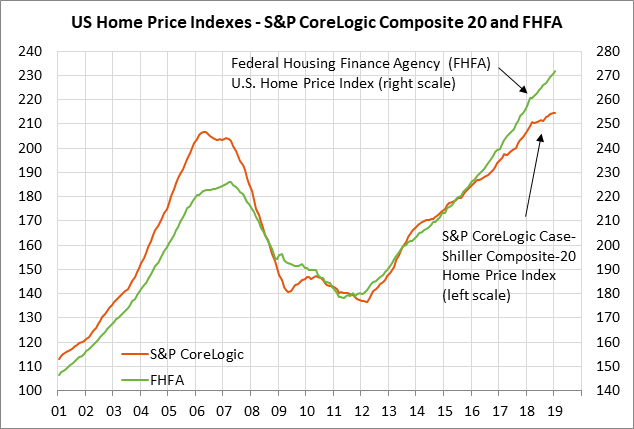

U.S. home prices expected to show another sharp rise — The consensus is for today’s Feb FHFA house price index to show a sharp increase of +0.6% m/m, matching Jan’s increase of +0.6% m/m. Home prices perked up in early 2019 due to an increase in home sales stemming from lower mortgage rates. The FHFA index was up by +5.6% y/y in January.

2-year T-note auction to yield near 2.39% — The Treasury today will sell $40 billion of 2-year T-notes. The $40 billion size of today’s auction is unchanged from the last four monthly 2-year auctions but is much larger than the $26 billion size that prevailed in 2015-17. The Treasury will then continue this week’s $133 billion T-note package by selling $20 billion of 2-year floating-rate notes and $41 billion of 5-year T-notes on Wednesday and $32 billion of 7-year T-notes on Thursday.

The 2-year T-note yield is currently trading at 2.39%, which is up by +23 bp from the late-March 14-month low of 2.16% but down by -58 bp from last November’s 10-3/4 year high of 2.97%. The +23 bp rise in the 2-year T-note yield seen in the past several weeks has been driven mainly by a less dovish view of Fed policy. The market is now expecting 36 bp of Fed rate cuts through the end of 2020 (according to the Dec 2020 federal funds futures contract), which is much less than the peak of 63.5 bp worth of expected Fed rate cuts seen several weeks ago (on March 27).

The 12-auction averages for the 2-year are as follows: 2.65 bid cover ratio, $360 million in non-competitive bids to mostly retail investors, 2.9 bp tail to the median yield, 25.0 bp tail to the low yield, and 47% taken at the high yield. The 2-year T-note is the least popular security among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of only 45.2% of the last twelve 2-year T-note auctions, which is far below the median of 62.1% for all recent Treasury coupon auctions.