- U.S. stock market buoyed by possible delay of auto tariffs and progress on Mexico/Canada metal tariffs

- PM May will make last-ditch effort at Brexit passage in early June

- Italian-German bond spread rises to 3-month high on increased Italian political risks

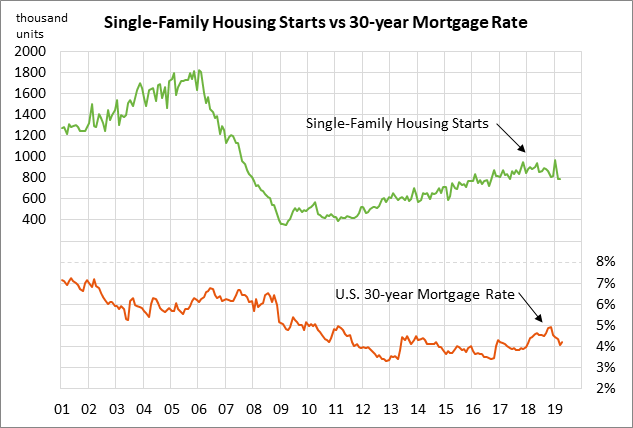

- Housing starts expected to improve on lower mortgage rates

U.S. stock market buoyed by possible delay of auto tariffs and progress on Mexico/Canada metal tariffs — The S&P 500 index on Wednesday continued to rebound higher from Monday’s 6-week low and closed the day up +0.58%, adding to Tuesday’s +0.80% recovery. The S&P 500 index on Monday’s 6-week low corrected lower by -5.2% from the early-May record high.

The U.S. stock market on Wednesday was encouraged by the Bloomberg report that President Trump will delay the tariffs on imported autos by up to 6 months. Bloomberg reported that news based on “people close to the discussions.” President Trump has until this Saturday (May 18) to announce a decision on the tariffs, i.e., whether or not to impose the tariffs or whether to delay a decision.

Bloomberg reported that USTR Lighthizer has been urging President Trump to delay the auto tariff decision to allow trade negotiations to proceed with Japan and Europe. EU Trade Commissioner Malmstrom reiterated this week that the EU will be ready with retaliatory tariffs on 20 billion euros of U.S. goods if Mr. Trump goes ahead with tariffs on imported EU vehicles.

The markets on Wednesday also received favorable news on the trade front when Treasury Secretary Mnuchin told a Senate panel that the Trump administration is close to an understanding with Mexico and Canada about removing tariffs on steel and aluminum. Some Senate Republicans have told the Trump administration they will not support the passage of Nafta 2.0 unless those tariffs are dropped.

With the positive trade news on Wednesday, the Trump seems to be trying to clear the deck of the auto tariffs and the Mexico-Canadian steel-aluminum tariffs so they can concentrate their firepower on ramping up Chinese tariffs to try to pressure China into a trade deal. President Trump spent much of his time earlier this week trying to calm down the U.S. stock market after its plunge on the collapse of any near-term US/Chinese trade deal.

The U.S. stock market would likely react very negatively if President Trump were to go ahead with the tariffs on U.S. auto imports due to the heavy hit that would cause for the important global auto industry. In addition, U.S. auto tariffs would attract a new set of retaliatory tariffs from affected nations and would also poison the US/Japan and US/EU trade talks that are just getting off the ground.

PM May will make last-ditch effort at Brexit passage in early June — Prime Minister May said that Parliament will vote on the Brexit withdrawal agreement bill in the first week of June. The Labour Party on Wednesday said that it would not support the bill since cross-party talks have been fruitless, but left open the possibility that it might abstain, possibly allowing the bill to pass.

If Parliament fails to approve the bill in early June, then the bill cannot be brought up again for a vote without starting a new session of Parliament. That would bring its own set of problems including the fact that the Conservative Party would be forced to renew support from the Northern Ireland DUP party, which might not be forthcoming. In reality, a Parliamentary defeat of the Brexit bill in early June might finally end Ms. May’s reign as Prime Minister. The party is already very close to changing the rules so that Ms. May is subject to a Tory leadership vote before December.

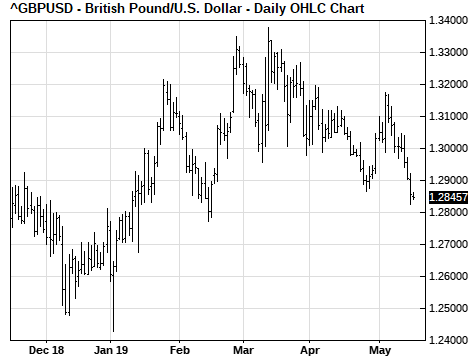

If Ms. May loses her job, then it seems likely that she will be replaced by a Conservative Party leader who is more hawkish on Brexit, thus increasing the risks for a no-deal Brexit when the deadline arrives on October 31. Sterling yesterday fell to a 3-month low as the Brexit situation looks increasingly unsolvable except through a new general election or a no-deal Brexit. Sterling is down -1.2% so far this week, adding to last week’s loss of -1.3%.

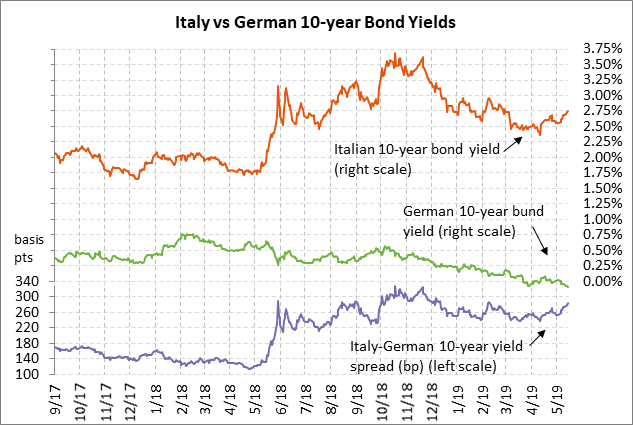

Italian-German bond spread rises to 3-month high on increased Italian political risks — The Italian-German bond yield spread on Wednesday rose to a 3-month high of 285 bp and has now risen by about 30 bp just in the past two weeks. However, the spread is still 42 bp below the 6-year high of 327 posted in late 2018 when Italy and the EU were arguing over the 2019 Italian budget.

Italian Deputy Prime Minister Salvini on Tuesday said that he would be open to breaking the EU’s budget deficit and national debt limits if necessary to boost employment. That threat seemed to be a play for votes at next week’s elections for the EU Parliament. However, the markets are worried that Mr. Salvini is planning to force a snap election in September in an attempt to gain more power and force the Five Star party out of the coalition.

If there are elections in September or October, then there may be no seated Italian government to prepare the 2020 budget. That would raise the odds of another Italian/EU standoff over the 2020 budget. The populist government largely lost last year’s battle with the EU over the budget, but not before Italian interest rates soared and helped cause a technical economic recession in the second half of 2018 with -0.1% q/q GDP growth in both Q3 and Q4.

Housing starts expected to improve on lower mortgage rates — The consensus is for today’s April housing starts report to show a solid gain of +6.2% to 1.209 million following March’s weak report of -0.3% to 1.139 million. U.S. home builder confidence is improving as seen by the fact that yesterday’s May NAHB housing market index rose by +3 points to a 7-month high of 66. The housing sector has been boosted by the sharp drop in the 30-year mortgage rate by 84 bp to the current level of 4.10% from the 8-year high of 4.94% posted last November.