- Markets wait for the official White House order that auto tariffs will be delayed

- No-deal Brexit preparations need to accelerate now that the UK will get a new PM

- U.S. consumer sentiment expected to slightly weaken

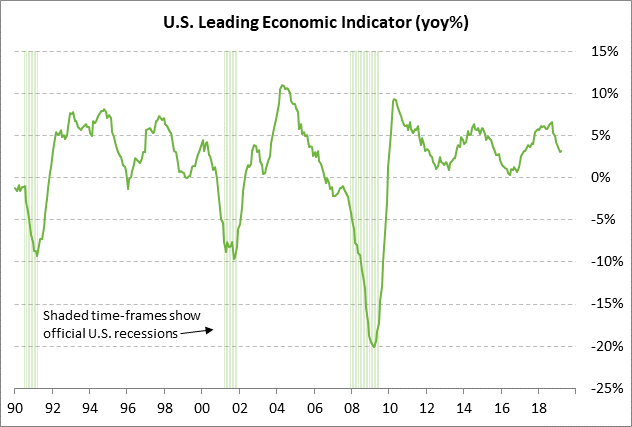

- U.S. LEI expected to show a small increase

Markets wait for the official White House order that auto tariffs will be delayed — The markets are waiting for an official announcement from the White House on the decision on tariffs on auto imports, which is due by tomorrow (Dec 18). Bloomberg on Thursday extended its reporting after having seen the draft executive order on the auto tariffs, which Bloomberg said would be signed this week according to unnamed sources.

Bloomberg said that President Trump’s order will give the EU and Japan 180 days to agree to a deal that would “limit or restrict” U.S. auto imports. The fact that President Trump is giving Japan and the EU six months to agree to a deal is positive in that the markets presumably won’t have to worry about those tariffs being imposed until at least December. However, there is no guarantee that President Trump might not halt the negotiations sooner if they are not going well and instead move ahead with the tariffs.

In addition, the odds of a final deal may not be high considering that the U.S. is demanding that the EU and Japan substantially reduce their auto exports to the U.S. in return for nothing except to avoid the threat of tariffs. Moreover, President Trump’s predilection for tariffs suggests that he would be just as happy to use tariffs to cut U.S. auto imports as he would using quotas, which means that Mr. Trump may try to drive a harder quota bargain than is acceptable to the EU and Japan.

Another factor that could prevent a deal is if the U.S. continues to insist that agriculture be part of the US/EU and US/Japanese trade talks. The EU refuses to talk about agriculture at all and Japan has refused to go any farther on agriculture concessions that were contained in the Trans-Pacific Partnership that went ahead without the U.S. If the U.S. insists on agriculture concessions, the US/Japan and US/EU trade talks might collapse.

There is reason for a little bit of optimism about a deal, however, since there are reports that USTR Lighthizer is not as worried about EU and Japanese auto imports as President Trump, suggesting that Mr. Lighthizer might try to push through only a mildly hawkish deal that is just enough to placate Mr. Trump and get the topic off the table. That is particularly the case if the US/Chinese trade war continues to rage during the rest of this year since the Trump administration views the trade battle with China as much more important than the auto-trade deficit with Japan and the EU. The U.S. clearly wants to train most of its firepower on China.

No-deal Brexit preparations need to accelerate now that the UK will get a new PM — Prime Minister May on Thursday agreed to leave her job with a timetable to be set in early June after Parliament votes on the Brexit withdrawal agreement bill. Ms. May will leave her job regardless of whether the vote on the bill is yes or no. The jockeying to become the new Prime Minister started immediately with Boris Johnson announcing that he is running.

The odds that Parliament will approve the Brexit bill in the first week of June appear to be nil. With Ms. May leaving shortly after the vote, the Labour Party can be assured that any deal they reach with Ms. May to support Brexit would be quickly jettisoned by the next Prime Minister. The Labour Party is therefore indicating that it will vote against the bill, assuring that the bill will receive the same fate as the last three votes.

The next Conservative Party leader is likely to be more hawkish on Brexit than was Ms. May. The key for the Conservative Party at this point is to simply get Brexit over with in order to stop the political hemorrhaging, perhaps even if that involves a no-deal Brexit on October 31. Boris Johnson, for one, seems to be willing to accept a no-deal Brexit if the EU will not bend to UK demands for a Brexit withdrawal agreement. The October 31 deadline is still a long way away, but the odds for a no-deal Brexit nevertheless went up yesterday with the news that UK will get a new and presumably more hawkish Prime Minister on Brexit.

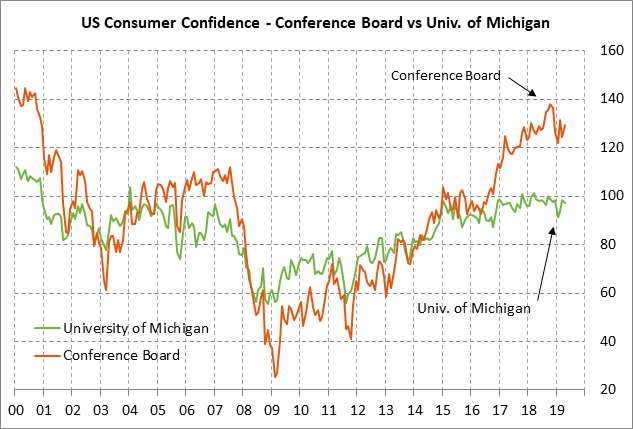

U.S. consumer sentiment expected to slightly weaken — The market consensus is for today’s University of Michigan U.S. consumer sentiment index to show a small -0.1 point decline to 97.1, adding to April’s -1.2 point drop to 97.2. The consumer sentiment index in April remained generally strong and was only -4.2 points below the 15-year high of 101.4 posted in March 2018. The markets will be watching today’s consumer sentiment report carefully following Wednesday’s disappointing April retail sales report of -0.2% m/m and +0.1% ex-autos, which was substantially weaker than market expectations of +0.2% and +0.7% ex-autos.

U.S. consumer sentiment remains generally strong due to (1) the strong U.S. labor market and rising wages, and (2) strength in household wealth with the stock market only moderately below recent record highs and with housing prices continuing to rise. However, consumer sentiment has recently run into some challenges from (1) Washington political strife after the release of the Mueller report, (2) the decline in the U.S. stock market on the worsening of the US/Chinese trade war, and (3) high gasoline prices on the successful OPEC+ production-cut agreement and supply disruptions for Iran and Venezuela.

U.S. LEI expected to show a small increase — The consensus is for today’s April leading indicators report to show a small increase of +0.2% m/m, adding to March’s increase of +0.4%. The LEI showed virtually no growth from October 2018 through February 2019 but finally showed a decent increase of +0.4% in March. The consensus is for U.S. Q3 GDP to dip to +2.0% from Q1’s +3.2%.