- May U.S. retail sales expected to rebound from April’s weakness

- U.S. consumer sentiment expected to back off from 8-month high but remain strong

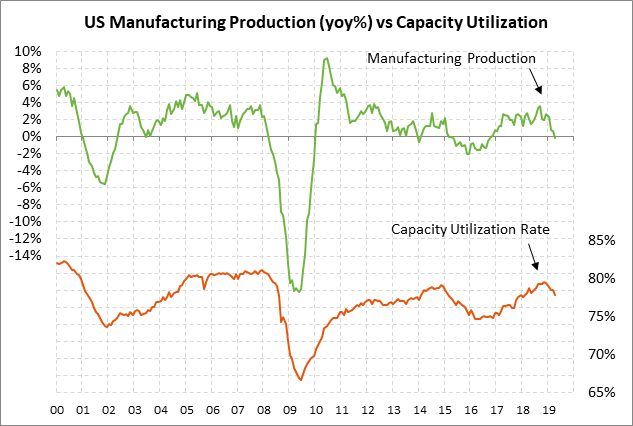

- U.S. manufacturing production expected to show the first increase of the year

- Boris Johnson handily wins first round of Conservative Party voting

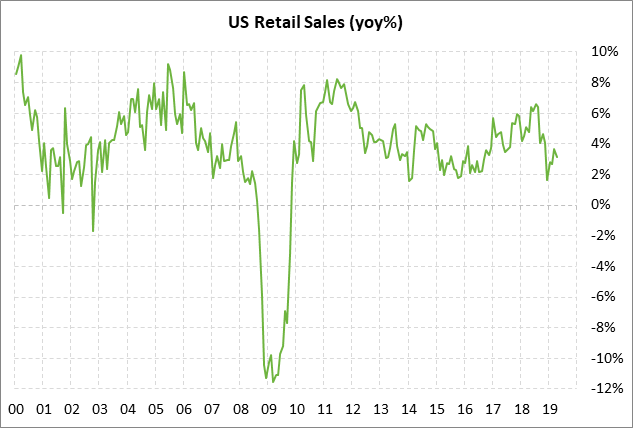

May U.S. retail sales expected to rebound from April’s weakness — The market consensus is for today’s May retail sales report to be strong at +0.6% and +0.4% ex-autos, improving substantially from April’s weak report of -0.2% and +0.1% ex-autos.

Retail sales have been very choppy in recent months with alternating months of strength and weakness. Since last August, however, retail sales have eked out an average monthly increase of only +0.1% m/m. In Q1, personal spending added only 0.90 percentage points to the Q1 GDP growth figure of +3.1%, well below the average of 2.20 points seen in the last three quarters of 2018.

Consumers in 2018 spent liberally due to the strong labor market and the 2018 tax cut that put more cash in the pockets of most taxpayers. However, consumer spending has slowed in recent months as the effects of the tax cut dissipated and as consumers became more cautious about the economic outlook after the Q4 slump in stocks and the recent weaker economy.

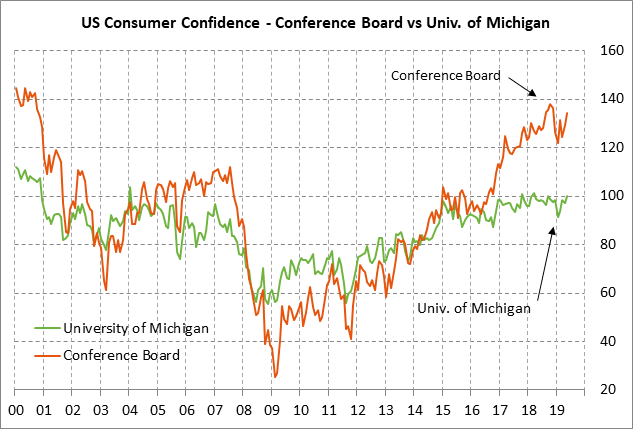

U.S. consumer sentiment expected to back off from 8-month high but remain strong — The consensus is for today’s preliminary-June University of Michigan U.S. consumer sentiment index to show a -2.0 point decline to 98.0, giving back most of May’s unexpected +2.8 increase to an 8-month high of 100.0. The consumer sentiment index remains in very strong shape at only 1.4 points below the 15-year high of 101.4 posted in March 2018.

U.S. consumer sentiment remains strong due to (1) the tight labor market and rising wages, (2) strong household wealth due to the generally strong U.S. stock market and rising home prices, and (3) the prospects for falling gasoline prices in coming weeks due to the recent -20% plunge in oil prices. Negative factors for consumer sentiment include (1) Washington political uncertainty, (2) some concern about higher consumer prices from tariffs, and (3) the heavy flooding seen in many areas this spring and the hard-hit farm sector from flooding and tariffs.

U.S. manufacturing production expected to show the first increase of the year — The consensus is for today’s May manufacturing production report to show a rise of +0.1% m/m, recovering part of April’s -0.5% decline. Meanwhile the consensus for the overall May industrial production report is for an increase of +0.2%, recovering part of April’s -0.5% decline.

U.S. manufacturing production in 2019 has yet to show a monthly increase and is down by a total of -1.6% so far this year. Manufacturing confidence has been sagging with the ISM manufacturing index showing back-to-back declines totaling -3.2 points in April/May and a decline in May to a 2-1/2 year low of 52.1.

The U.S. manufacturing sector is being hurt by weak consumer spending in recent months and by reduced business investment as executives deal with the uncertainty of tariffs and their supply chains. Weak manufacturing is also a problem in Europe where the Eurozone April industrial production report on Thursday fell -0.5% m/m, which was the biggest decline in 4 months. Weaker global manufacturing activity has mainly been due to tariffs and trade tensions.

Boris Johnson handily wins first round of Conservative Party voting — Boris Johnson handily won Thursday’s first round of voting by Conservative Party MPs with 114 votes, which was more than 2-1/2 times the second place finisher of Jeremy Hunt with 43 votes. Michael Gove won 27 votes and Dominic Raab won 27 votes. Also making the cut with a handful of votes were Sajid Javid, Matt Hancock, and Rory Stewart. There were three candidates that were eliminated from the contest on Thursday: Andrea Leadsom, Mark Harper, and Esther McVey.

The seven remaining candidates will be put to the test with progressive rounds of voting next Tuesday through Thursday in order to whittle the list down to just two candidates. Those two candidates will then be voted on by some 160,000 Conservative Party members across the country. The new leader and Prime Minister is expected to be named in the week of July 22.

The betting probability for Boris Johnson to win rose to 82% on Thursday from 73% on Wednesday after his solid showing in Thursday’s first round of voting. His challengers are far behind with Jeremy Hunt at 10%, Michael Gove at 4%, and the others with even lower probabilities. There is little doubt that Boris Johnson will be the next Prime Minister unless he commits some epic gaffe in the last few weeks of the contest.

With the outcome of the race virtually certain, the markets are mainly focused on Boris Johnson’s view of no-deal Brexit. He dialed down his threats for a no-deal Brexit this week but the markets cannot shake the view that a no-deal Brexit is substantially more likely under Boris Johnson than under Theresa May. Mr. Johnson has staked virtually all of his credibility on his promise to take the UK out of the EU by the deadline of October 31. A no-deal Brexit could turn out to be the only way to fulfill that promise since Parliament has failed three times to approve the only withdrawal deal that the EU says it will offer.

After he becomes Prime Minister, Mr. Johnson will huff and puff at EU officials for a rewrite of the withdrawal agreement, but there is no sign that EU officials will concede. That would leave a no-deal Brexit as the only real choice, other than deferring the deadline again and calling new elections, which could result in the decimation of the Conservative Party based on current polls.