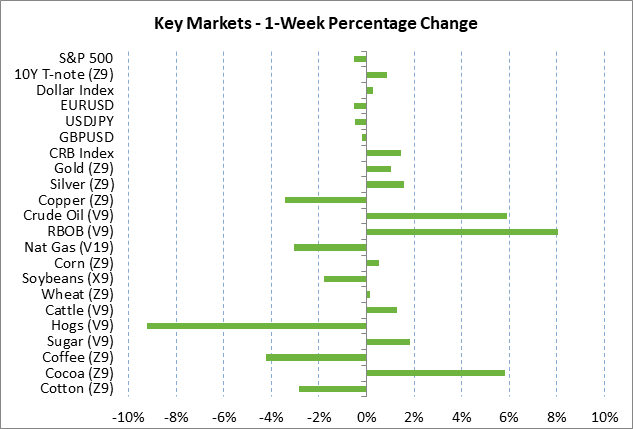

- Weekly market focus

- Markets await Oct 10 high-level US/Chinese trade meeting

- Fed battles money market squeeze this week with term repos

- Senate will consider CR this week to prevent government shutdown next week

Weekly market focus — The U.S. markets this week will focus on (1) US/Chinese trade relations as the markets look ahead to the high-level meeting expected for around Oct 10, (2) whether the Fed is successful this week with its repos in calming the money market squeeze that began last week, (3) a busy week for Fed-speak with 11 appearances by various Fed officials after last week’s Fed dots suggested that most Fed members are not expecting any more rate cuts, (4) geopolitical affairs as the world’s leaders gather this week in New York for the UN General Assembly meetings, (5) oil prices as the markets wait to see if there will be any military retaliation for the Sep 14 attack on key Saudi oil facilities and how quickly Saudi Arabia can fully restore its production, (6) the Treasury’s sale of $131 billion of T-notes this week, and (7) this week’s earnings reports from 11 of the S&P 500 companies.

The European markets this week will focus mainly on Brexit as UK/EU negotiations over the Irish border backstop continue and as the UK Supreme Court early this week is expected to issue a ruling on the legality of UK Prime Minister Johnson’s suspension of Parliament until Oct 14. Today’s Eurozone Sep Markit Eurozone manufacturing PMI is expected to show a small +0.3 point increase to 47.3, adding to Aug’s +0.5 increase to 47.0 but remaining below the expansion-contraction level of 50.0.

The Asian markets will continue to focus mainly on US/Chinese trade relations, which took a turn for the worse last Friday after President Trump said he wasn’t interested in a partial deal.

Markets await Oct 10 high-level US/Chinese trade meeting — The U.S. and China both called last week’s deputy-level meetings in Washington “constructive.” China said the high-level trade meeting that the markets have been expecting is being planned for about Oct 10.

However, the market’s view of US/Chinese trade relations took a turn for the worse last Friday after President Trump said that he wasn’t interested in “a partial deal” with China and wants a permanent deal. That knocked down market hopes that the two sides might be moving towards a plan for a “mini-deal” or “interim” deal whereby President Trump would agree to defer the upcoming Oct 15 and Dec 15 tariffs, and possibly roll back the Sep 1 tariff, in return for Chinese ag purchases and commitments on IP protection. The prospects seem dim for a full US/Chinese trade deal anytime in the near future.

The markets were also discouraged last Friday when China announced only an hour after Mr. Trump’s comment that he wasn’t interested in a partial deal that the planned goodwill tour by a Chinese delegation of U.S. farms had been canceled. China said the cancelation of the farm tour wasn’t related to the status of the trade talks, but it seemed clear that China was signaling there will be no major thaw on Chinese ag purchases until President Trump agrees to roll back at least some tariffs.

Separately, the markets are waiting to see if the U.S. and Japan can meet their self-imposed deadline of producing a final US/Japan trade agreement for this week when there could be a Trump/Abe meeting at the UN meetings in NY.

Fed battles money market squeeze this week with term repos — The Fed last Friday announced that it will conduct daily repos of at least $75 billion through October 10. The Fed said it will also conduct 14-day term repos with an aggregate amount of at least $30 billion this Tuesday, Thursday and Friday (Sep 24, 26 and 27).

The Fed’s repo operations will provide short-term liquidity to the financial system and presumably bring short-term money market rates back down to normal levels after last week’s squeeze that sent the repo rate as high as 10%. The effective federal funds rate last Friday was at 1.90%, which was a bit high at 2.5 bp above the 1.875% mid-point of the new funds rate target range of 1.75%-2.00% and 10 bp above the new IOER rate (interest on excess reserves) of 1.80%. The repo rate last Friday fell back to the more normal level of 2.65% from 4% after the Fed announced the upcoming repo operations, which assured the markets that liquidity will be forthcoming.

There was a technical squeeze on short-term liquidity last week caused by the settlement of Treasury auctions and the withdrawal of cash from the banking system by corporations to make their Sep 15 tax payments. Liquidity over the near-term will be further aggravated by next Monday’s (Sep 30) end-of-quarter statement date and by the settlement of this week’s Treasury auctions.

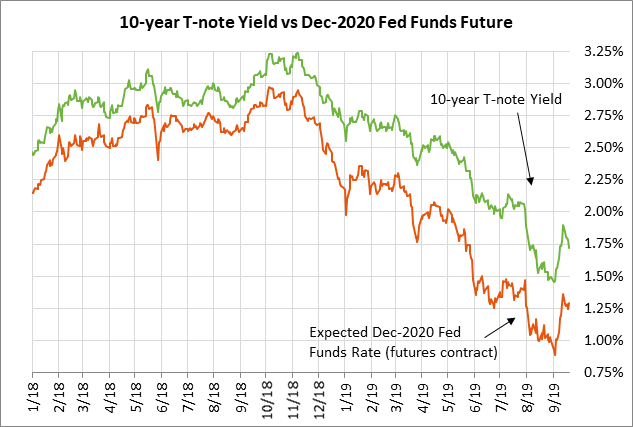

Last week’s money market squeeze had consequences for the Treasury market and dollar funding rates, but did not have any implications for short-term Fed policy. The Fed last week met market expectations by cutting its funds rate target by -25 bp to 1.75%/2.00% and the IOER rate by -30 bp to 1.80%. In the bigger picture, the markets are now expecting the FOMC to soon produce a plan on how it will deal with the new chronic shortage of reserves, with options including (1) boosting its balance sheet by buying T-bills or T-notes, (2) running more frequent daily repo operations, or (3) setting up a standing repo facility to help dealers fund their growing cache of Treasury securities as the federal budget deficit rises.

Senate will consider CR this week to prevent a government shutdown next week — The Senate this week is expected to pass the same bipartisan continuing resolution (CR) that the House passed last week to fund the government through Nov 21 and prevent a government shutdown next Tuesday (Oct 1). However, a larger showdown and a government shutdown is still possible when the CR expires on Nov 21 over issues such as border wall funding.