- Weekly global market focus

- Q1 earnings season kicks into high gear

- U.S. stock and bond markets continue to hinge on trade tensions, oil, and interest rates

- Markit U.S. PMI reports expected mixed

- U.S. existing homes sales expected to remain strong

Weekly global market focus — The U.S. markets this week will focus on (1) trade tension developments, (2) this week’s visits by Macron and Merkel to Washington and whether they have any success in reducing U.S.-European trade tensions or improving the prospects for the Iranian nuclear deal, (3) interest rates as the Treasury auctions $113 billion of T-notes this week and as the 10-year T-note yield is close to challenging the 3.00% yield level, (4) a heavy dose of Q1 earnings, (5) this week’s busy economic calendar, which is capped by Friday’s Q1 GDP report (expected +2.0%), and (6) oil prices, which reached a new 3-1/4 year high last week on falling global oil inventories and fears that President Trump will withdraw from the Iranian nuclear agreement on his May 12 deadline.

The markets this week will continue to closely watch U.S.-Chinese trade tensions as reports emerged last week that the U.S. Treasury is considering using its authority under the U.S. International Emergency Economic Powers Act to block China from investing in the U.S. tech sector as part of the Trump administration’s sanctions on China for IP violations. Mr. Trump’s 25% tariff on $50 billion worth of Chinese imports is still in the 60-day comment period. China last week shut down $1.1 billion of U.S. sorghum exports to China with a 179% anti-dumping tariff in retaliation for earlier U.S. tariffs on solar and washing machine imports. Treasury Secretary Mnuchin over the weekend tried to soothe market nerves by saying that he is considering making a trip to China to address trade tensions.

This will be European-relations week in Washington with French President Macron visiting the U.S. on Monday through Wednesday and with German Chancellor Merkel meeting with President Trump at the White House on Friday. Key events during Mr. Macron’s 3-day visit include (1) policy talks on Tuesday followed by President Trump’s first state dinner, and (2) an address by Mr. Macron to a joint session of Congress on Wednesday.

In Europe, the focus will mainly be on Thursday’s ECB meeting where the ECB could adopt more neutral policy guidance language. This is a busy week for European economic data with PMI reports today, confidence data on Tuesday, and inflation and GDP data on Friday. The markets will continue to watch the Italian political situation where there has been virtually no progress towards forming a government. This will be a busy earnings week with 131 of the Euro Stoxx 600 companies scheduled to report.

In Asia, the focus will mainly be on (1) trade tensions, (2) the North Korean situation as South and North Korean leaders hold a summit on Friday, (3) the Thursday/Friday BOJ meeting, which is expected to produce an unchanged policy, and (4) this Sunday night’s Chinese PMI reports.

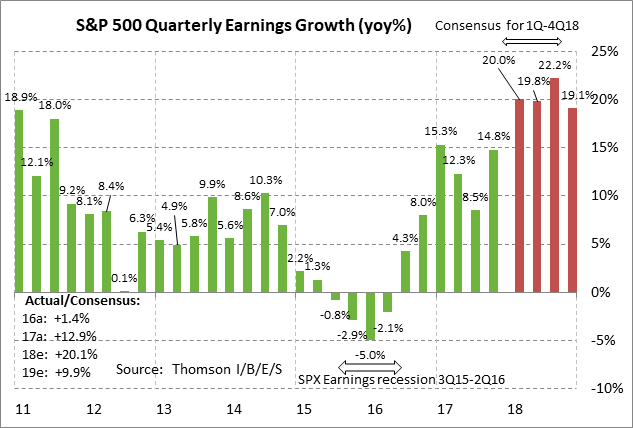

Q1 earnings season kicks into high gear — Q1 earnings season kicks into high gear this week with 180 of the S&P 500 companies scheduled to report. Q1 earnings expectations are so high that positive earnings results have been only mildly rewarded while disappointments have produced sharp sell-offs. Of the 87 SPX companies that have reported, 79.3% have announced above-consensus earnings, which is above the long-term average of 64% and the 4-quarter average of 75%, according to Thomson I/B/E/S. Of reporting companies, 71.3% have announced above-consensus revenue, which is above the long-term average of 60% and the 4-quarter average of 69%.

The market consensus is for Q1 SPX earnings growth of +20.0% (+18.3% ex-energy), which is better than expectations of +18.5% as of April 1 (prior to the beginning of earnings season). The market is expecting strong earnings growth to continue with SPX earnings growth of +19.8% in Q2, +22.3% in Q3, and +19.1% in Q4, according to Thomson I/B/E/S. On a calendar year basis, the consensus is for earnings growth of 20.1% in 2018 and +9.9% in 2019.

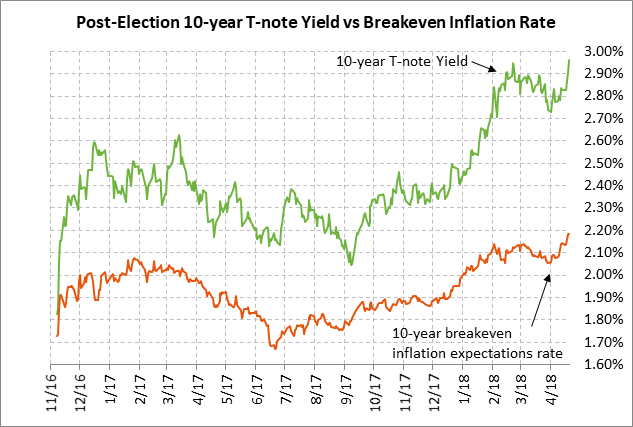

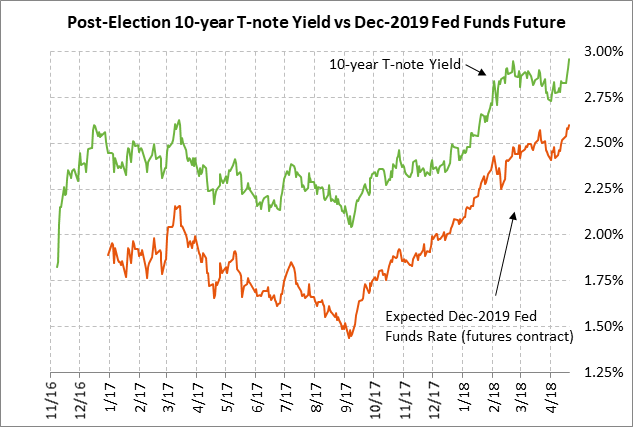

U.S. stock and bond markets continue to hinge on trade tensions, oil, and interest rates — U.S. stocks are currently seeing support from strong Q1 earnings results but there are still substantial bearish factors including trade tensions and rising interest rates. The 10-year T-note yield last Friday rose to a new 4-1/4 year high of 2.96%. The markets anticipate a challenge of the psychological 3.00% level. A rise in the 10-year yield above the 6-3/4 year high of 3.05% posted in Jan 2014 would be particularly bearish development.

The 10-year T-note yield has risen due to higher inflation expectations and more hawkish Fed expectations. The 10-year breakeven rate last week rose to a new 3-3/4 year high of 2.19% due to (1) last Thursday’s new 3-1/4 year high of $69.56 per barrel in May crude oil prices, and (2) rising commodity prices due in part to tariffs and sanctions. Meanwhile, market expectations last Friday for Fed rate hikes through 2019 rose to a new record high of 97.5 bp (3.9 rate hikes), helping to push the 2-year T-note yield to a new 9-1/2 year high of 2.46%.

Markit U.S. PMI reports expected mixed — Today’s Apr Markit PMI reports are expected to show cautious business confidence with the manufacturing PMI expected to fall -0.4 to 55.2 (after March’s modest +0.3 increase) and the services PMI expected to rise slightly by +0.1 to 54.1 (after March’s -1.9 point drop).

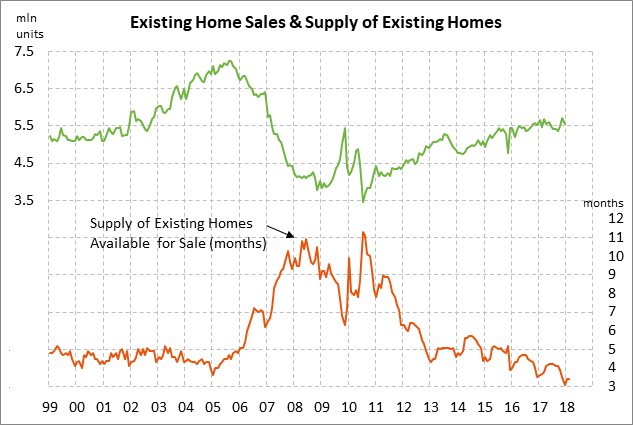

U.S. existing homes sales expected to remain strong — The market consensus is for today’s Mar existing home sales report to show a small +0.2% increase to 5.55 million, adding to Feb’s +3.0% increase to 5.54 million. Home sales remain in strong shape at only -3.1% below Nov’s 11-year high of 5.72 million units. Home sales have been curbed somewhat by tight supplies and rising mortgage rates.