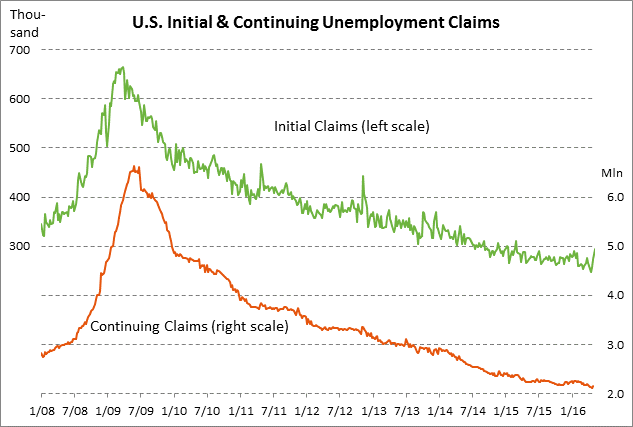

- Today’s report will help determine if 3-week rise in initial claims is just temporary

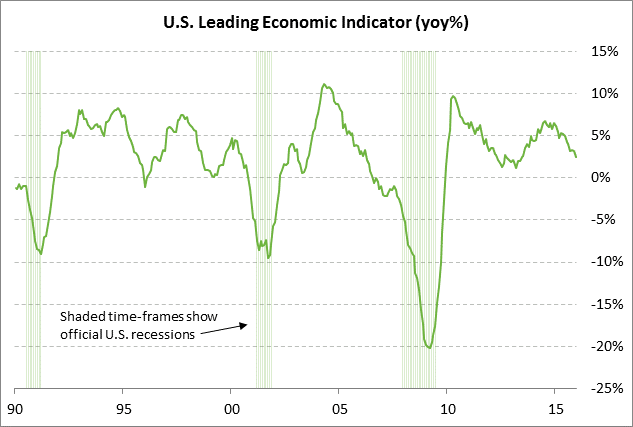

- LEI expected to improve to +0.4% and support expectations for stronger Q2 GDP growth

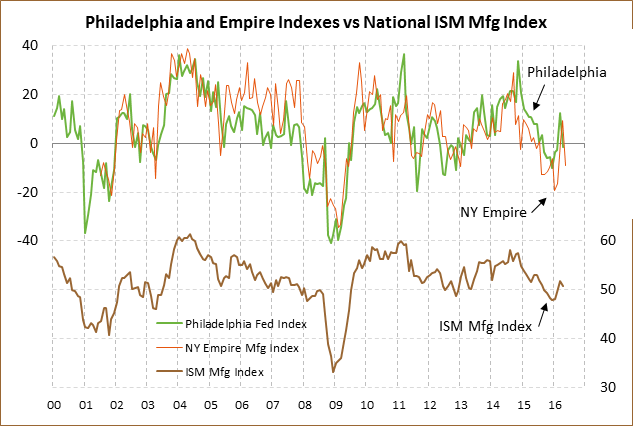

- Philadelphia Fed index expected to rise back into positive territory

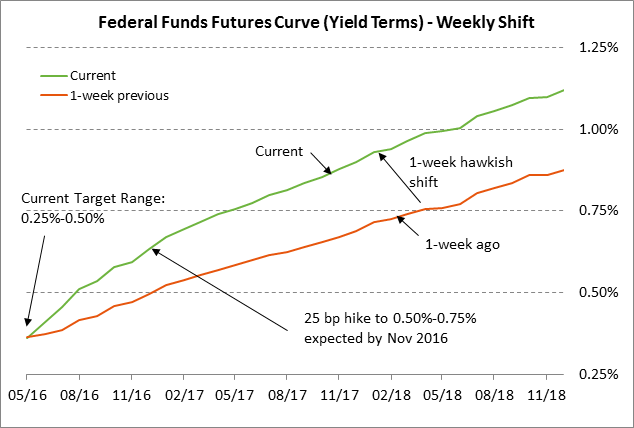

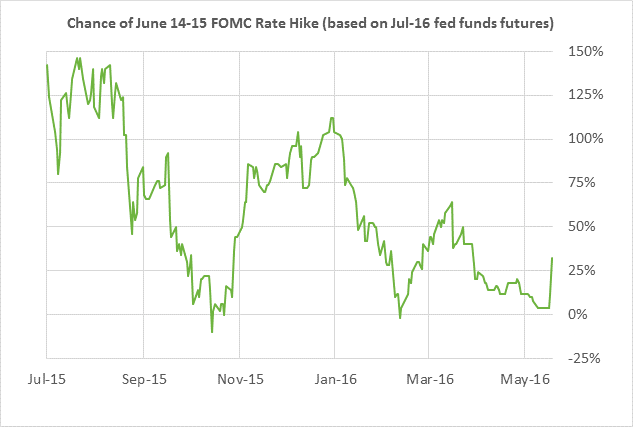

- Probability of June Fed rate hike jumps further after hawkish FOMC minutes

- 10-year TIPS

Today’s report will help determine if 3-week rise in initial claims is just temporary — The markets are a little concerned about the 3-week rise of +46,000 in initial unemployment claims to a 1-1/4 high of 294,000. Most of last week’s +20,000 rise was concentrated in New York, which suggested that it was tied to a strike at Verizon and possibly the timing of school holidays. Indeed, the market is expecting today’s initial claims report to fall by -19,000 to 275,00, almost exactly reversing last week’s +20,000 increase. Nevertheless, the 3-week rise in initial unemployment claims comes after the weak April payroll report of +160,000, which raised concerns that the U.S. labor market might be slowing. The markets in any case will remain extremely vigilant on the labor front.

Meanwhile, the continuing claims series remains in good shape so far at 2.161 million, just +37,000 above the previous week’s 15-1/2 year low of 2.124 million. The market is expecting today’s continuing claims report to show a -3,000 decline to 2.158 million, falling back a bit after last week’s +37,000 increase to 2.161 million.

LEI expected to improve to +0.4% and support expectations for stronger Q2 GDP growth — The market is expecting today’s April leading indicators report to show a solid increase of +0.4%, improving from March’s +0.2% increase. Before March’s +0.2% increase, the LEI fell in the previous three months (Dec-Feb) by a total of -0.5%, presaging the weak Q1 GDP report of +0.5%. A strong LEI report today would support the recent optimism for an upward rebound in GDP in Q2 sparked in part by the +1.3% surge in April retail sales. The Atlanta GDPNow model is currently forecasting Q2 GDP at +2.5%.

Philadelphia Fed index expected to rise back into positive territory — The market is expecting today’s May Philadelphia Fed business outlook index to show a +4.6 point increase to 3.0, reversing about one-third of April’s sharp -14.0 point decline to -1.6. The Philadelphia Fed index has been weak in recent months, having been in negative territory in 7 of the last 8 months. The index rose by +15.2 to 12.4 in March but then gave up most of that gain by falling -14.0 in April to -1.6. Today’s Philadelphia Fed index will be only the second piece of business confidence data to be released thus far for May. The first piece of May business confidence data, the May Empire index, fell by -18.58 to -9.02, kicking off the May data on a weak note.

Probability of June Fed rate hike jumps further after hawkish FOMC minutes — The federal funds futures market yesterday pushed the odds for a rate hike at the upcoming June 14-15 FOMC meeting to 32% from 12% on Tuesday and only 4% on Monday. The April 26-27 FOMC minutes released yesterday indicated that FOMC members were “leaving open the possibility” of a June rate hike if the economy picked up, the labor market strengthens, and inflation makes progress towards reaching the Fed’s +2.0% target. The hawkish FOMC minutes followed the warning by Fed Presidents Lockhart and Williams on Tuesday that the markets were underestimating the risks of a near-term rate hike and that the Fed might raise rates as many as three times this year.

Even though the FOMC in the April minutes left open the possibility of a rate hike in June, the actual decision will turn on whether the Fed’s various conditions have been met. April retail sales showed a very encouraging increase of +1.3% and Q2 GDP growth at present is on track to reach +2.5% after the very poor +0.5% growth rate hike in Q1. In addition, Tuesday’s April CPI report showed a +0.4% y/y increase. However, the March payroll report of +160,000 was poor and initial unemployment claims have jumped in the past three reporting weeks. As such, the U.S. economic data cannot be considered uniformly strong enough to produce a strong certainty about a June rate hike. There is also the caveat that the June 14-15 FOMC meeting comes a week before the June 23 Brexit vote, which if it goes the wrong way could spark a big sell-off in the UK and European financial markets.

The advantage of a Fed rate hike in June is that Fed Chair Yellen is scheduled to hold a press conference after the meeting where she could elaborate on the reasons for a Fed rate-hike decision. Still, we think the Fed is once again talking tough and acting weak, and will not raise rates at the June meeting. However, a July rate hike has now become much more likely since it has become more obvious that the Fed is chomping at the bit to move ahead with its rate-hike regime. The federal funds futures market is now discounting the likelihood of a Fed rate hike at the July meeting at 54%, up from 20% on Monday.

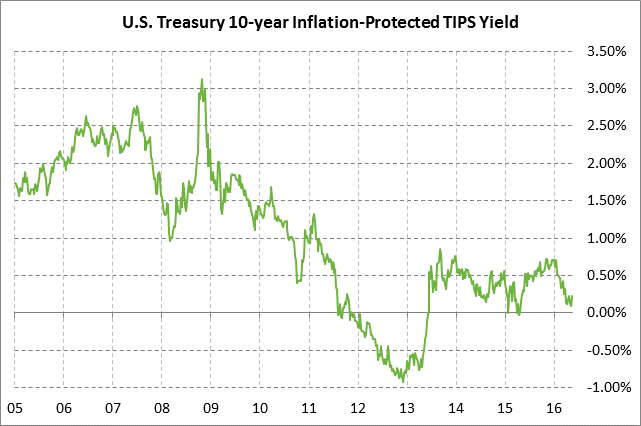

10-year TIPS auction — The Treasury today will sell $11 billion of 10-year TIPS. Today’s 10-year TIPS auction will be the second and final reopening of the 5/8% 10-year TIPS note of Jan 2026 that the Treasury first sold in January. Today’s 10-year TIPS issue was trading at 0.22% in when-issued trading late yesterday afternoon.

The 12-auction averages for the 10-year TIPS are as follows: 2.40 bid cover ratio, $27 million in non-competitive bids, 6.7 bp tail to the median yield, 15.0 bp tail to the low yield, and 50% taken at the high yield. The 10-year TIPS is the most popular coupon security among foreign investors and central banks. Indirect bidders, a proxy for foreign buying, have taken an average of 64.1% of the last twelve 10-year TIPS auction, which is well above the average of 56.0% for all recent Treasury coupon auctions.