- Yellen’s testimony indicates Fed is highly uncertain

- U.S. existing home sales expected to post new 9-1/4 year high

- U.S. house prices expected to rise another +0.6%

- Betting odds on Brexit continue to strongly favor Remain vote while public opinion polls are tied

- 7-year T-note auction to yield near 1.50%

- 30-year TIPS auction to yield near 0.90%

- Weekly EIA report

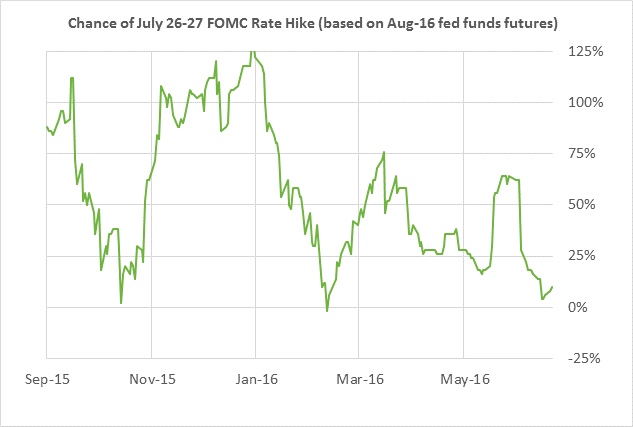

Yellen’s testimony indicates Fed is highly uncertain — Fed Chair Yellen today will testify before the House Financial Services Committee, repeating her written remarks from yesterday before the Senate Banking Committee but taking different questions from committee members. Ms. Yellen in her testimony yesterday expressed uncertainty, not only about the potential impact of tomorrow’s Brexit vote, but also about the weak U.S. May payroll report, poor U.S. productivity and low U.S. business investment. Even if the UK on Thursday votes to remain within the EU, Ms. Yellen made clear that the Fed now has a number of concerns about the U.S. economy that will delay the Fed’s next rate hike.

The federal funds futures curve showed only a slight 1-2 bp upward move in response to Ms. Yellen’s testimony, indicating that the markets were not at all surprised by Ms. Yellen’s uncertain and dovish tone. The federal funds futures market is currently discounting the odds for a rate hike at only 10% for the next FOMC meeting on July 26-27 and at 34% for the following meeting on Sep 20-21.

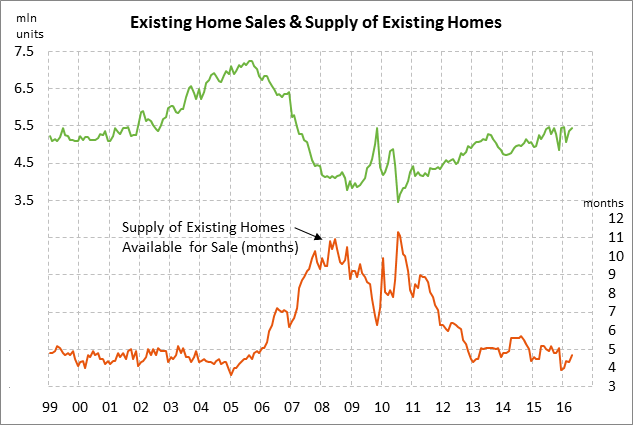

U.S. existing home sales expected to post new 9-1/4 year high — The market is expecting today’s May existing home sales report to show an increase of +1.8% to 5.55 million units, adding to April’s +1.7% increase to 5.45 million. Existing home sales in March-April rose by a total of +7.4%, roughly reversing the -7.3% decline seen in February. The March existing home sales level of 5.45 million is only -0.6% below the 9-1/4 year high of 5.48 million units posted last summer in July 2015. Today’s expected increase of +1.8% to 5.55 million would put the series at a new 9-1/4 year high, illustrating the current strength in home buying activity.

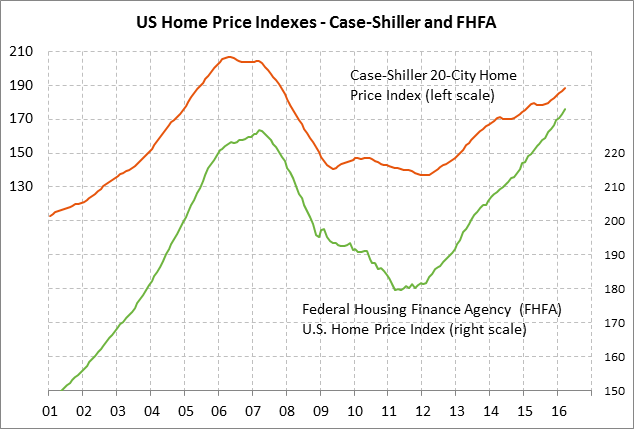

U.S. house prices expected to rise another +0.6% — The market is expecting today’s April FHFA U.S. house price index to show another strong increase of +0.6%, adding to March’s increase of +0.7%. The FHFA house price series continues to march higher, not having shown a decline in 4-1/2 years. The series is up by +30% from the housing bust low posted in March 2011 and is up by +6.1% y/y. Home prices continue to see strength based on strong demand, mildly tight supplies, and low mortgage rates.

Betting odds on Brexit continue to strongly favor Remain vote while public opinion polls are tied — The markets yesterday continued to be in a better mood about Thursday’s Brexit vote than they have been in the past several weeks. The “poll of polls” compiled by the website WhatUKThinks.org yesterday moved slightly in the Remain direction with 51% in the Remain camp versus 49% in the Leave camp, versus the 50%-50% reading on Monday. The betting odds yesterday were unchanged from Monday with a 78% probability for a Remain vote versus a 5% probability for a Leave vote, according to oddschecker.com. The polls continue to indicate that the undecideds remain high at nearly 15% of potential voters, indicating that the outcome will be decided by how those undecided voters break at the last minute.

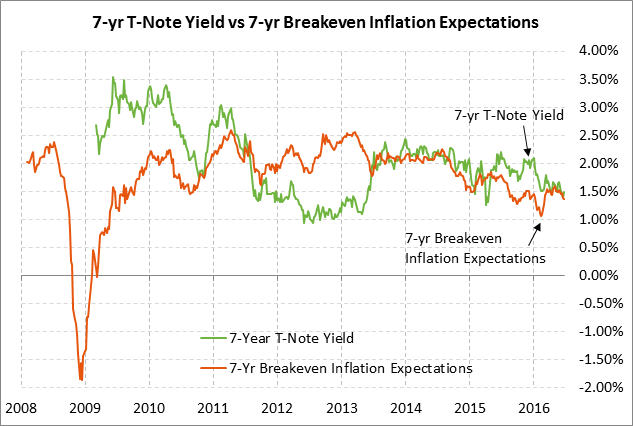

7-year T-note auction to yield near 1.50% — The Treasury today will conclude this week’s $106 billion coupon package in time for Thursday’s Brexit vote by selling $13 billion of 2-year floating rate notes, $28 billion of 7-year T-notes, and $5 billion of 30-year TIPS.

Today’s 7-year T-note issue was trading at 1.50% in when-issued trading late yesterday afternoon, which translates to an inflation-adjusted yield of 0.14% against the current 7-year breakeven inflation expectations rate of 1.36%. The 12-auction averages for the 7-year are as follows: 2.49 bid cover ratio, $19 million in non-competitive bids to mostly retail investors, 4.2 bp tail to the median yield, 14.1 bp tail to the low yield, and 48% taken at the high yield. The 7-year is slightly above average in popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, took an average of 57.9% of the last twelve 7-year T-note auctions, which is slightly above average of 57.0% for all recent Treasury coupon auctions.

30-year TIPS auction to yield near 0.90% — Meanwhile, the benchmark 30-year TIPS was trading at 0.90% late yesterday afternoon. Today’s auction will be the first reopening of the 1% 30-year TIPS of Feb 2046 that the Treasury first sold earlier this year in February. The Treasury follows a yearly pattern of selling a new TIPS issue in February and then reopening that issue with auctions in June and October. The 12-auction averages for the 30-year TIPS are as follows: 2.51 bid cover ratio, $15 million in non-competitive bids, 7.3 bp tail to the median yield, 14.9 bp tail to the low yield, 47% taken at the high yield, and 58.7% taken by indirect bidders (moderately above the average of 57.0% for all recent coupon auctions).

Weekly EIA report — The market consensus for today’s weekly EIA report is for a -1.5 million bbl decline in U.S. crude oil inventories, an unchanged level of Cushing crude oil inventories, a -1.15 million bbl drop in gasoline inventories, a +1.0 million rise in distillate inventories, and a +0.6 point increase in the refinery utilization rate to 90.8%. U.S. crude oil remains in a massive glut with inventories at +32.9% above the 5-year seasonal average. Product inventories are more than ample with gasoline inventories at +10.7% above average and distillate inventories at +19.7% above average. Meanwhile, U.S. crude oil production in last week’s report fell by -0.3% to a new 1-3/4 year low of 8.716 million bpd, down by a total of -9.1% from the 44-year high of 9.610 million bpd posted a year ago in June 2015.