- FOMC minutes will be watched for rate-hike timing, fiscal uncertainty, and any balance sheet discussions

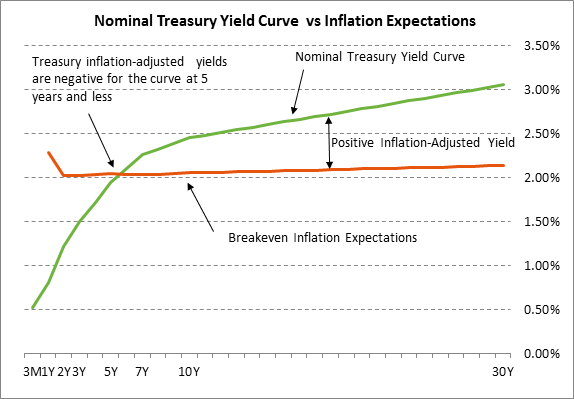

- Real yields remain negative on the Treasury curve shorter than 5 years

- 5-year T-note auction to yield near 1.92%

- U.S. existing home sales expected to show continued strong home demand

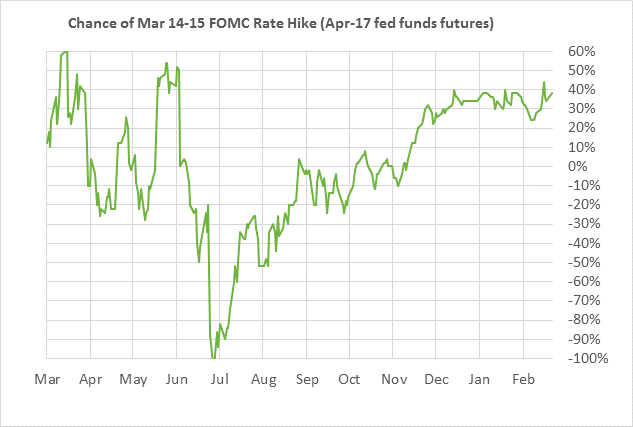

FOMC minutes will be watched for rate-hike timing, fiscal uncertainty, and any balance sheet discussions — The markets will be dissecting today’s minutes from the Jan 31/Feb 1 FOMC meeting mainly for any hints on the timing of the Fed’s next rate hike. The federal funds futures market is currently discounting a 36% chance of a rate hike at the next FOMC meeting on March 14-15, about a two-thirds chance of a rate hike by the June 13-14 meeting, and a 100% chance of a rate hike by the June 13-14 meeting.

The market last week tightened up expectations for Fed policy after Fed Chair Yellen’s mildly hawkish testimony to Congress and after strong CPI and retail sales reports. Ms. Yellen last week said that the Fed’s inflation and labor market goals are “very close” to being met.

On the issue of fiscal uncertainty, Ms. Yellen last week said that “Considerable uncertainty attends the economic outlook” and that there will be “possible changes to US fiscal and other policies.” Nevertheless, she suggested that the Fed would go ahead with rate hikes in the future if required by the Fed’s dual labor-inflation targets even if the Fed did not know exactly what would transpire on the fiscal front.

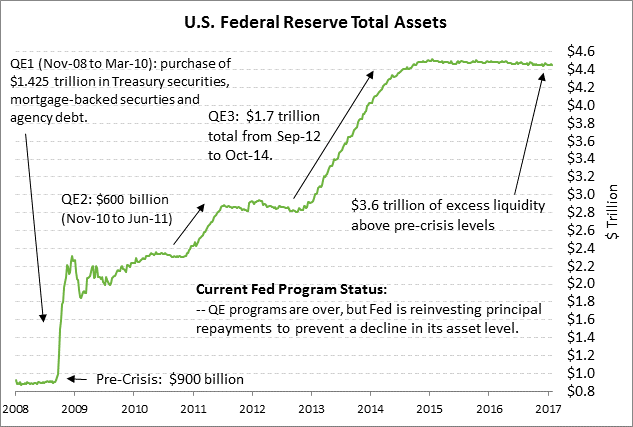

The markets will also be dissecting the FOMC minutes for any discussions about the Fed’s balance sheet. When asked about the topic in her Congressional testimony last week, Ms. Yellen simply reiterated the Fed’s current balance sheet policy stance, which is that the Fed will maintain its existing policy of reinvesting principal payments from maturing securities in new securities until the process of interest rate normalization is “well underway.” The markets are generally not expecting any change to the Fed’s reinvestment policy until 2018 or even 2019, but the markets are looking for the Fed to discuss its balance sheet policy in more depth in coming months.

The topic of the Fed’s balance sheet has become a hotter issue now that three of the seven Fed governor chairs are available and are waiting to be filled by President Trump. President Trump, if he follows through on his seemingly hawkish stance on the Fed, could appoint new Fed governors who favor a quicker start on drawing down the Fed’s balance sheet. President Trump also has the opportunity to replace Ms. Yellen as Fed Chair in Feb 2018 and Stanley Fischer as Vice Chair in June 2018. A shift to a more hawkish Fed composition could open the door to a slow draw-down in the Fed’s balance sheet as soon as next year.

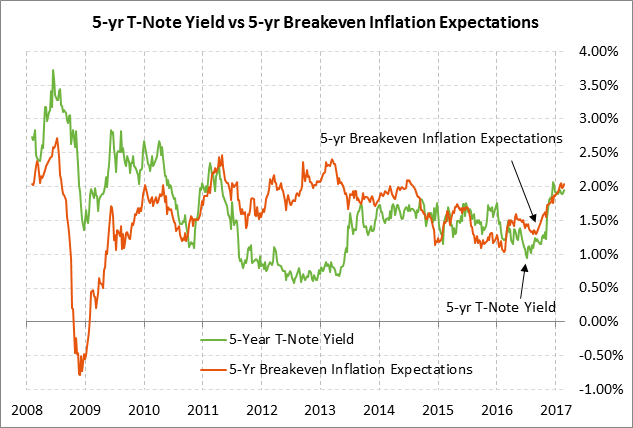

Real yields remain negative on the Treasury curve shorter than 5 years — The Treasury yield curve of 5 years and shorter remains below inflation expectations, indicating how the shorter end of the yield curve remains artificially low. The current 2-year T-note yield of 1.21%, for example, is 84 bp below the 2-year breakeven inflation rate of 2.05%. The 5-year T-note yield of 1.92% is slightly below the 5-year breakeven inflation rate of 2.02% by 10 bp.

Investors will not accept negative inflation-adjusted yields forever and short-term yields will eventually have to move back above inflation expectations. However, that process will likely take at least several more years since it will require (1) a more robust economy offering higher real yields, (2) a normalization of Fed policy with the Fed raising its federal funds rate target to a positive spread above inflation, and (3) reduced safe-haven demand for Treasury securities.

5-year T-note auction to yield near 1.92% — The Treasury today will sell $34 billion of 5-year T-notes and $13 billion of 2-year floating-rate notes. The Treasury will then conclude this week’s $101 billion T-note package by selling $28 billion of 7-year T-notes on Thursday.

The benchmark 5-year T-note late yesterday closed at 1.92%, which translates to an inflation-adjusted yield of -0.10% against the current 5-year breakeven inflation expectations rate of 2.02%.

The 12-auction averages for the 5-year T-note are as follows: 2.45 bid cover ratio, $44 million in non-competitive bids, 4.9 bp tail to the median yield, 13.5 bp tail to the low yield, and 48% taken at the high yield. The 5-year is moderately popular among foreign investors and central banks. Indirect bidders, a proxy for foreign buying, have taken an average of 62.2% of the last twelve 5-year T-note auctions, moderately above the average of 59.1% for all recent Treasury coupon auctions.

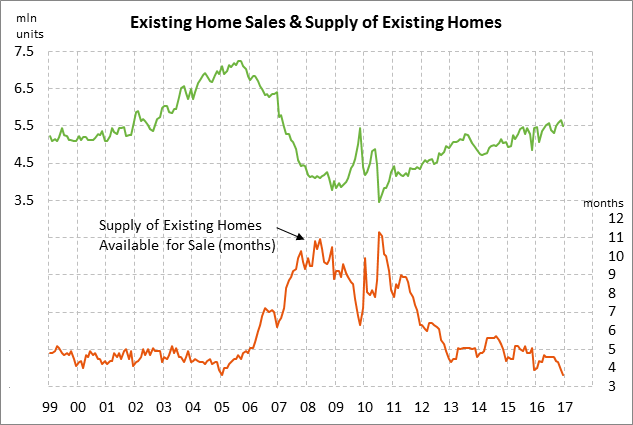

U.S. existing home sales expected to show continued strong home demand — The market is expecting today’s Jan existing home sales report to show an increase of +0.9% to 5.54 million, recovering about a third of December’s -2.8% decline to 5.49 million. U.S. home sales remain in generally strong shape since the December figure was only -2.8% below the 9-3/4 year high of 5.65 million units posted in November. U.S. home sales would likely be even stronger if there were more homes available for sale. There were only 3.6 months worth of home available for sale in December, the lowest level in 12 years.

Home sales are likely to dampened somewhat over the near-term by (1) the tight availability of homes, (2) rising home prices (up 35% from the recession trough), and (3) rising mortgage rates. The current 30-year mortgage rate of 4.15% is up by 61 bp from the pre-election level of 3.54%. However, demand for homes is likely to remain firm in coming months since consumers have gained confidence about the economy and the labor market. Moreover, many potential home buyers likely recognize that interest rates are likely to go up in coming years, meaning this still a good time to buy a home.