- Weekly market focus

- Yellen effectively pre-announces a rate hike for next week

- U.S. factory orders expected to show a solid gain

Weekly market focus — Market attention this week will focus on (1) anticipation of next week’s FOMC meeting after Fed Chair Yellen last Friday effectively pre-announced a rate hike for that meeting, (2) this Friday’s Feb unemployment report, which is expected to show a solid +185,000 gain in payrolls and a rise in average hourly earnings to +2.8% y/y from Jan’s +2.5%, (3) any developments on a Republican corporate tax reform plan, (4) the Treasury’s sale of $56 billion of 3, 10 and 30-year securities, and (5) a light SPX earnings schedule with only 6 of the S&P 500 companies scheduled to report this week.

On the Washington front, the House this week will continue working on its Obamacare repeal-and-replace legislation as House Speaker Ryan tries to meet his goal of getting House approval of the plan within three weeks. Mr. Ryan is trying to get Obamacare off his plate so he can focus on the budget and corporate tax reform. The debt ceiling suspension expires next Wednesday (March 15) but Congressional action will not be necessary on a debt ceiling hike until summer as the Treasury’s uses its usual emergency measures.

The overseas markets are focused (1) European politics as the Netherlands holds its national election next Wednesday where the anti-euro and anti-immigrant Freedom Party has seen its lead dwindle, (2) the French election where National Front leader Marine Le Pen is holding her polling strength, and (3) Thursday’s ECB meeting where the ECB is expected to leave its policy rates unchanged and affirm its intention to keep its QE program intact through year-end.

Chinese Premier Li Keqiang on Sunday released a new set of economic targets as the week-long National People’s Congress began. The new GDP growth target is “around 6.5%, or higher if possible,” which is slightly weaker than the 2016 target of 6.5-7.0%. The “higher if possible” phrase was apparently added for a bit of optimism as the Chinese government tries to keep the economy stable through the end of this year when President Xi Jinping will consolidate his leadership control at the twice-a-decade Communist Party Congress in Q4. The new GDP target in our view will not do much to reduce the pressure on government officials to fudge the GDP numbers and use artificial and unsustainable means to stimulate the Chinese economy.

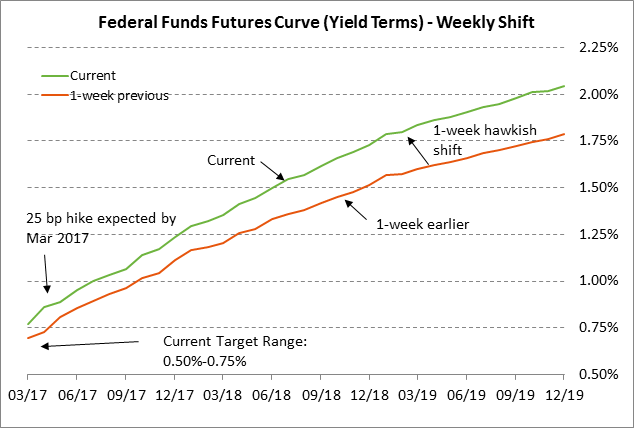

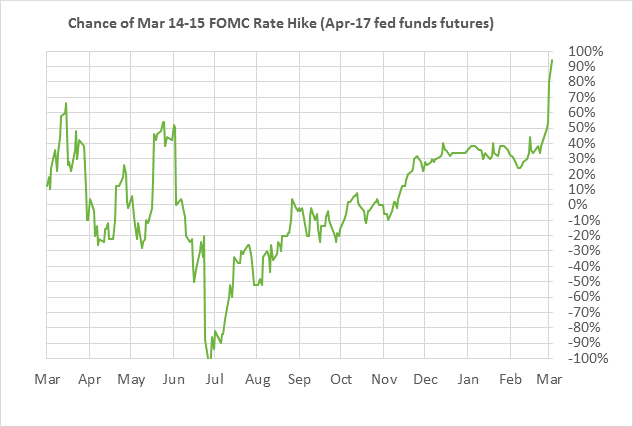

Yellen effectively pre-announces a rate hike for next week — Just a week-and-a-half ago on Friday, Feb 24, the market was discounting only a 40% chance of a rate hike at next week’s FOMC meeting. However, market expectations for that rate hike quickly ramped up to 94% last week due to hawkish comments by every Fed official that spoke last week.

The clincher then came last Friday when Ms. Yellen effectively pre-announced a rate hike for next week. Ms. Yellen said that a rate hike next week would be “likely appropriate” if the economy evolves as the Fed expects. That meant that barring some unforeseen economic disaster the Fed at its 2-day meeting next Tue/Wed will raise its funds target range by 25 bp to 0.75-1.00%.

Ms. Yellen presumably already knows that she has the votes for a rate hike or she would not have made such a confident statement about a rate hike for next week. Fed Vice Chair Stanley Fischer on Friday said that Ms. Yellen typically “does not tend to make decisions that ignore the views of the rest of the committee.”

The market discussion about the Fed last week shifted very quickly from a 50-50 debate about whether the Fed would raise interest rates next week to a lock on a rate hike and a discussion about whether the Fed has already fallen behind the curve on raising interest rates. The Fed seems to have shifted its outlook on monetary policy very quickly, raising questions about whether the Fed is getting a little panicky about whether it has already fallen behind the curve. Ms. Yellen last Friday tried to downplay those concerns by staying that she does not believe the Fed is behind the curve and that she still sees interest rates rising at a gradual rate.

Nevertheless, the Fed’s quick decision on a rate hike for next week accelerated market expectations for Fed rate hikes in the future as well. The market is now discounting the odds for the Fed’s second rate hike of the year at 62% for the July 25-26 meeting and at 100% for that rate hike by the time of the Sep 19-20 meeting (i.e., at either the July or Sep meeting). The market is then discounting a 68% chance of the Fed’s third rate hike of the year by the time of the Dec 12-13 FOMC meeting.

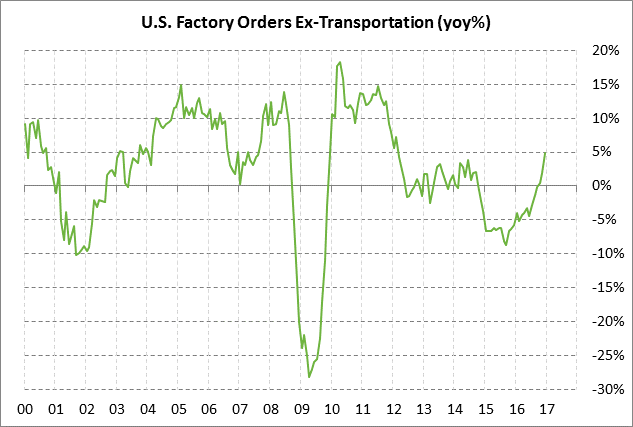

U.S. factory orders expected to show a solid gain — The market consensus is for today’s Jan factory orders report to show an increase of +1.0% following December’s report of +1.3% and +2.1% ex-transportation. Factory orders are finally starting to show some strength. Excluding the volatile transportation sector, factory orders have risen on a month-to-month basis for the last five consecutive months (Aug-Dec) and on a year-on-year basis reached a 4-3/4 year high of +4.8% y/y in December.

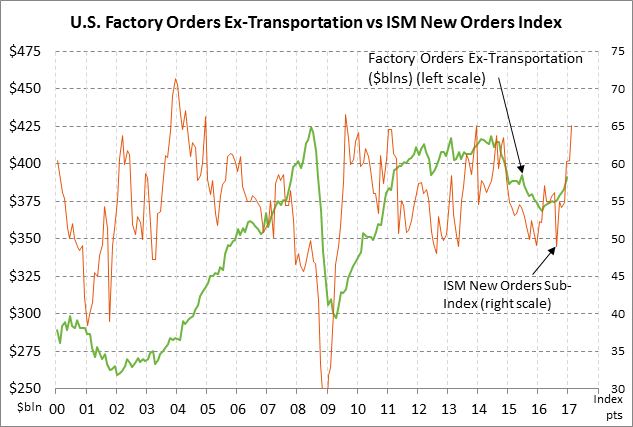

U.S. manufacturing executives are now the most optimistic about new orders since 2009. The ISM manufacturing new orders sub-index rose sharply by +4.7 points in February to 65.1, matching the 7-1/2 year high first posted in Dec 2013. Positive factors for manufacturing orders include (1) expectations for increased business investment after the Republican sweep of Washington and the promises for corporate tax reform and a big infrastructure spending program (2) improved overseas economic growth, (3) some recovery in the petroleum sector, and (4) continued strength in vehicle sales. The main headwind for manufacturing orders continues to be the strong dollar.