- 10-year T-note yield plumbs the bottom of its post-election range

- 10-year T-note auction to yield near 2.37%

- Job openings expected to remain strong

10-year T-note yield plumbs the bottom of its post-election range –The 10-year T-note yield last Friday posted a 4-1/2 month low of 2.269% on the overnight news of the U.S. missile strike on Syria and on Friday morning’s news that payrolls rose by only +98,000 (versus expectations of +180,000). However, the T-note yield then moved sharply higher in the early afternoon and closed the day up +4.1 bp at 2.382% after NY Fed President William Dudley recalibrated his recent comments to make clear that he was talking only about a very short pause in the Fed’s rate hike process when the Fed starts reducing its balance sheet. The 10-year T-note yield on Monday then gave back about half of Friday’s gains and closed down by -1.6 bp at 2.366%.

In the bigger picture, the 10-year T-note yield has fallen sharply by -23.4 bp since the March 14-15 FOMC meeting. The 10-year yield started falling after the meeting because the FOMC confirmed that it still expects three rate hikes per year over the next three years as opposed to fears by some that the Fed might move to four rate hikes. The 10-year yield fell further after the recent FOMC minutes said the Fed plans to start reducing its balance sheet later this year and after NY Fed President Dudley said the Fed might pause its rate hikes briefly when it starts reducing the balance sheet.

Other reasons behind the recent decline in the 10-year T-note yield include (1) weak Q1 U.S. economic data as the Atlanta Fed last Friday cut its U.S. Q1 GDP tracking estimate to +0.6% from +1.2% (although the NY Fed’s Nowcasting Q1 forecast is still strong at +2.8%), (2) reduced expectations for tax reform and fiscal stimulus after House Republicans were unable to pass an Obamacare repeal-and-replace bill, and (3) heavy short-covering in T-note prices by traders who were previously looking for a straight shot higher in T-note yields.

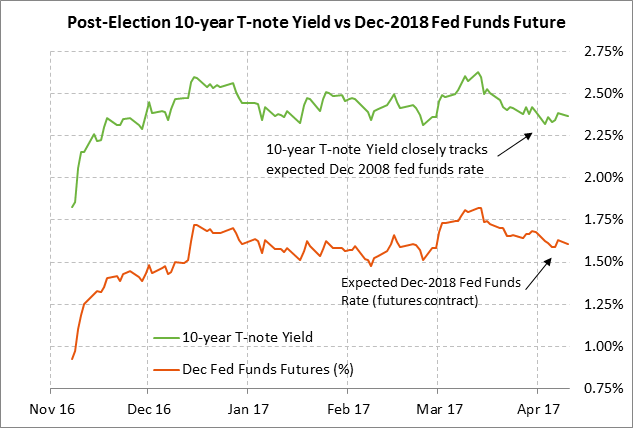

The nearby chart shows how closely the 10-year T-note yield has been tracking Fed rate-hike expectations, as reflected by the December 2018 federal funds futures contract (which is the expected average federal funds rate during the month of Dec 2018). Since the March 14-15 FOMC meeting, the 10-year T-note yield has fallen by -23.4 bp to 2.366%, which is close to the -21.5 bp drop in the Dec 2018 federal funds futures contract over the same time horizon.

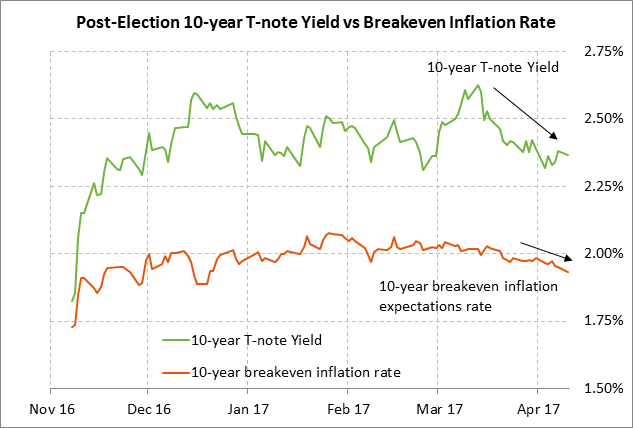

The 10-year T-note yield has also been pushed lower by the -6.2 bp drop in inflation expectations seen since the March 14-15 FOMC meeting. The 10-year breakeven inflation expectations rate last Friday fell to 3-1/2 month low of 1.925% and closed on Monday just +0.9 bp above that level at 1.934%.

There is the possibility that the 10-year T-note yield could fall farther considering that the 10-year yield is still 54 bp higher than it was before the election and that the Republican agenda has run into some serious roadblocks. T-note yields could fall farther since (1) tax reform is not likely to see much progress with Congress on recess through next week, (2) Friday’s retail sales report is expected to be weak, and (3) geopolitical safe-haven demand continues with uncertainty about North Korea and Syria.

However, renewed upward pressure on T-note yields could emerge in coming weeks since the Fed seems convinced that weak Q1 GDP is transitory and since the Fed still seems intent on executing its tightening plan for two more rate hikes by year end and balance sheet reduction starting “later this year.”

10-year T-note auction to yield near 2.37% — The Treasury today will sell $20 billion of 10-year T-notes in the second and final reopening of 2-1/4% 10-year T-note of Feb 2027 that the Treasury first sold in February. The Treasury will then conclude this week’s $56 billion coupon package by selling $12 billion of reopened 30-year T-bonds on Wednesday.

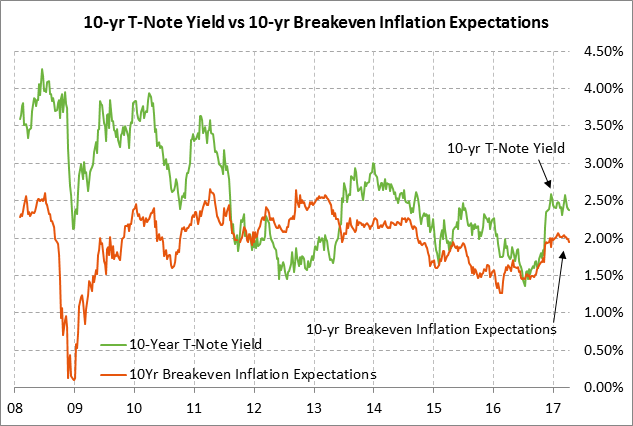

Today’s 10-year T-note issue was trading at 2.37% in when-issued trading late yesterday afternoon. That translates to an inflation-adjusted yield of 0.44% against the current 10-year breakeven inflation expectations rate of 1.93%. The 12-auction averages for the 10-year are as follows: 2.49 bid cover, $16 million in non-competitive bids, 5.0 bp tail to the median yield, 11.9 bp tail to the low yield, and 44% taken at the high yield.

The 10-year T-note is the fourth most popular security among foreign investors and central banks behind the 10-year TIPS, 30-year TIPS, and 7-year T-note. Indirect bidders, a proxy for foreign buyers, have taken an average of 65.2% of the last twelve 10-year T-note auctions, which is well above the average of 59.5% for all recent Treasury coupon auctions.

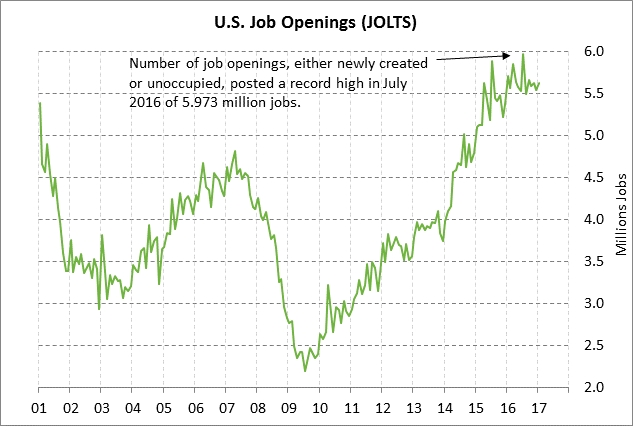

Job openings expected to remain strong — The market consensus is for today’s Feb JOLTS job openings report to show a +24,000 increase to 5.650 million jobs, adding to the +87,000 increase to 5.626 million seen in January. The series is close to the 12-month average of 5.61 million jobs and is much higher than the average of about 4.5 million jobs that was seen before the Great Recession. The continued high level of the JOLTS job openings series is a positive leading indicator for the payroll report since many job openings will turn into an actual job hire within 1-3 months when the hiring process is complete. The markets remain optimistic about the labor market despite last Friday’s March +98,000 payroll increase since that weak report was mainly due to winter storm Stella that hit the Northeastern U.S. during the payroll survey week.