- Chinese volatility continues with the yuan dropping to a 4-3/4 year low

- Brent oil prices fall below even the 2008 financial-crisis low but reduced petro-tax means brighter days down the road

- Elevated level of initial unemployment claims is not a concern given holiday distortions

- Dec 15-16 FOMC minutes are a bit dovish

Chinese volatility continues with the yuan dropping to a 4-3/4 year low — China’s Shanghai Composite stock index on Wednesday managed to close moderately higher by +2.25% and remain above Tuesday’s 2-1/2 month low. However, the Chinese yuan fell by -0.61% against the dollar to post a new 4-3/4 year low. The weaker yuan will help the Chinese economy and exporters by making Chinese exports cheaper. However, the weak yuan also encourages Chinese investors and businesses to shift capital out of China to avoid the effects of further yuan depreciation. There are concerns that the flight of capital from China could gain momentum, thus sapping the Chinese stock and bond markets of capital and Chinese industry of investment capital. Indeed, China saw an outflow of about $267 billion over the 3-month period of Sep-Nov as investors and businesses seek better returns outside China.

Brent oil prices fall below even the 2008 financial-crisis low but reduced petro-tax means brighter days down the road — Feb Brent crude oil prices on Wednesday plunged by -$2.11 (-5.79%) to $34.31 on technical selling and a bearish weekly EIA report. Feb Brent crude oil yesterday fell to a new 11-1/2 year low on the nearest-futures chart of $34.13, easily taking out even the 2008 financial-crisis low of $36.20 and falling to levels not seen since July 2004. Brent crude oil prices have now plunged by roughly 70% from the $110 level seen as recently as July 2015. Meanwhile, Feb WTI crude oil futures prices yesterday fell to a 5-year low of $33.77 but managed to remain slightly above the 2008/09 financial crisis low of $33.20.

The plunge in oil prices is alarming for the markets due to (1) the sharp drop in petroleum-sector stocks, (2) the negative fall-out for the U.S. economy from the worsening petroleum sector recession, (3) worries about more petroleum sector bankruptcies and fresh weakness in petroleum-sector junk bonds, and (4) concern about severe stress in various petro-countries around the world. However, the plunge in oil prices will eventually be a boon for the global economy as the plunge in fuel costs frees up cash for consumers and businesses and frees up more money for savings and investment. The plunge in fuel costs is essentially reducing the massive petro-tax that is extracted from the world economy every day of the year.

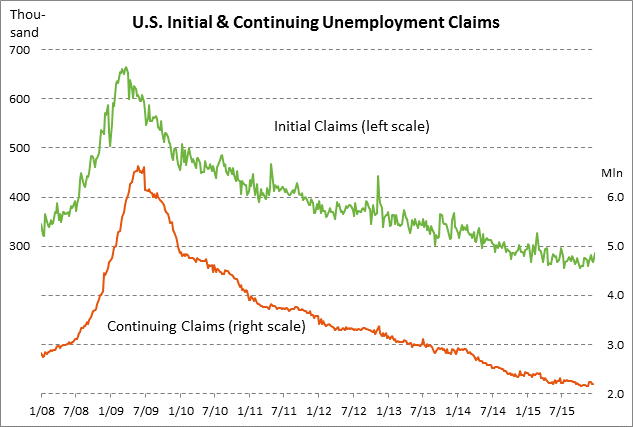

Elevated level of initial unemployment claims is not a concern given holiday distortions — The initial unemployment claims series is a bit elevated, but not by enough to cause any consternation about the labor market, particularly because the claims data is being jostled by holiday distortions. The initial claims series in last week’s report (for the week ended Dec 25) rose by +20,000, putting the series +32,000 above the 42-year low of 255,000 posted in July 2015. Meanwhile, the continuing claims series is +52,000 above the 15-year low of 2.146 million posted in Oct 2015. The market is expecting today’s initial claims report to show a -12,000 decline to 275,000 and today’s continuing claims series to show a +2,000 increase to 2.200 million.

On the labor front, the market is mainly looking ahead to Friday’s unemployment report. In that regard, yesterday’s Dec ADP report of +257,000 was stronger than market expectations of +195,000 and bolstered expectations for Friday’s payroll report.

The market is expecting Friday’s Dec payroll report to show an increase of +200,000, down mildly from Nov’s +211,000 and the 3-month moving average of +218,000. As long as monthly payroll growth remains near or above +200,000, the Fed will continue on a path of steadily raising interest rates. Meanwhile, the market is expecting Friday’s Dec unemployment rate to be unchanged from the 8-year low of 5.0% seen in Oct-Nov. That is only +0.3 points above the FOMC’s mid-point forecast of 4.7% for the unemployment rate in 2016-18, illustrating that the U.S. labor market has nearly met the FOMC’s long-term target.

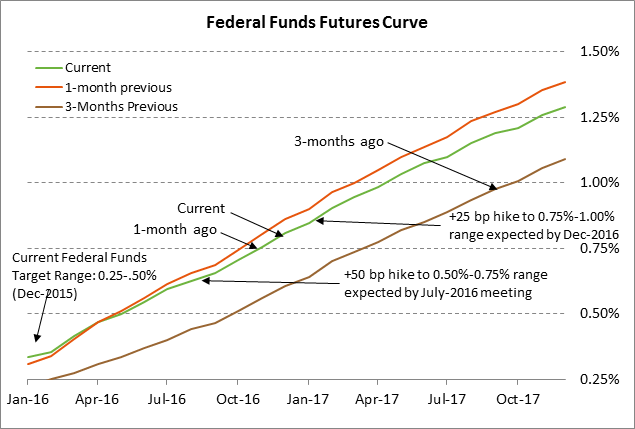

Dec 15-16 FOMC minutes are a bit dovish — The minutes of the Dec 15-16 FOMC meeting, which were released yesterday, indicated that some FOMC members saw the December rate hike as a “close call” even though all 10 voting FOMC members voted in favor of the rate hike. The minutes suggest that the FOMC as a whole is not in a hurry to raise interest rates farther. FOMC members in particular expressed concern that inflation is well below the FOMC’s target and some members were worried that the Fed’s inflation target might lose credibility. The core PCE deflator, which is the Fed’s preferred inflation measure, was stuck at only +1.3% y/y all during 2015, well below the Fed’s +2.0% inflation target.

The federal funds futures market is discounting only two rate hikes during 2016, the first by July and the second by December. However, many analysts are predicting as many as four rate hikes during 2016. Indeed, Fed Vice Chairman Stanley Fischer said yesterday that forecasts for only two rate hikes in 2016 are “too low” and that forecasts for four rate hikes in 2016 are “in the ballpark.” Of course, the FOMC in recent years has had to climb down from an overly hawkish position on numerous occasions due to overseas concerns (China, Europe), a soft U.S. economy and labor market, and low inflation. Indeed, the markets have a much better forecasting record than the Fed, which means it makes more sense to pay attention to the federal funds market than to the FOMC’s forecasts.